Introduction: From Cash to Cosmos — How India’s Fintech Revolution is Reshaping the Economy

India, a land of vibrant hues and bustling bazaars, is witnessing a silent revolution — a revolution not waged with swords or slogans, but with smartphones and algorithms. This is the rise of India’s fintech, a wave of innovation that is redefining how the nation interacts with money. Move over, dusty bank ledgers and serpentine queues; welcome to a world where instant digital payments, AI-powered loans, and seamless investments dance on the tip of your fingers.

This is not just an upgrade in convenience; it’s a tectonic shift in the landscape of the Indian economy. Imagine millions previously excluded from the formal financial system, now empowered with digital wallets and micro-loans. Picture small businesses thriving on crowdfunding platforms, and farmers accessing crop insurance with a single click. This is the canvas India’s fintech is painting, one pixel at a time.

But this revolution is not without its brushstrokes of challenge. Regulatory hurdles, data privacy concerns, and the digital divide threaten to dampen the vibrant colors of progress. Yet, the entrepreneurial spirit and government initiatives promise to keep the palette vibrant.

Driving Financial Inclusion: How Fintech is Bringing Millions into the Fold

Across India’s vast and diverse landscape, a quiet revolution is underway. Driven by the ingenuity of fintech, millions who were once financially invisible are being brought into the fold, gaining access to services that were previously out of reach. This surge in financial inclusion, particularly in rural areas, is reshaping the very fabric of the Indian economy, empowering individuals and igniting new possibilities.

Bridging the Gap: From Exclusion to Inclusion

For decades, remoteness, lack of documentation, and cumbersome procedures acted as insurmountable barriers for many Indians, particularly those in rural areas, to access basic financial services. Savings accounts, loans, and insurance remained distant dreams, hindering economic participation and perpetuating a cycle of poverty.

Enter the Fintech Revolution:

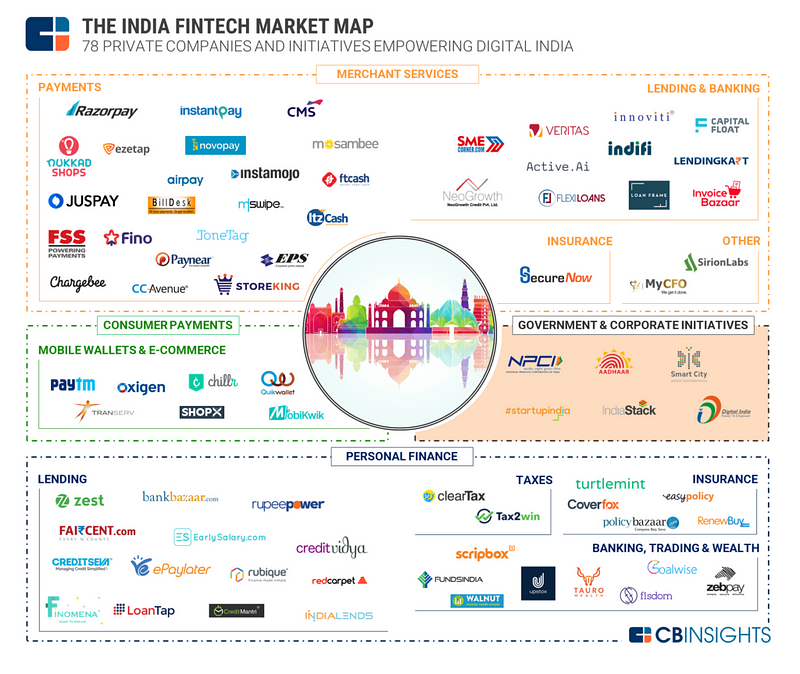

Fintech, with its tech-driven approach, is bridging this gap with innovative solutions tailored to the needs of the unbanked. Mobile wallets like Paytm and PhonePe have transformed smartphones into mini-banks, allowing for easy money transfers, bill payments, and even micro-savings. This has brought financial services directly into the hands of millions who previously lacked access to traditional banking infrastructure.

Beyond Payments: A Spectrum of Services

The fintech revolution extends far beyond just payments. Micro-lending platforms like Ujjivan Small Finance Bank and Jana Small Finance Bank are providing small, affordable loans to rural entrepreneurs and farmers, allowing them to invest in their businesses and livelihoods. AI-powered credit scoring is making these loans accessible even to those without formal credit history, fostering financial independence and growth.

Insurance for the Masses:

Insurance, once considered a luxury, is now becoming a reality for rural populations thanks to fintech. Companies like Acko and Go Digit offer micro-insurance products for crops, livestock, and even health, providing much-needed security against unforeseen risks. This newfound financial resilience is empowering communities and paving the way for long-term prosperity.

The Road Ahead: Challenges and Opportunities

While the progress is undeniable, challenges remain. Data privacy concerns, digital literacy gaps, and the need for robust regulatory frameworks are areas that require continuous attention. However, the potential of fintech to drive financial inclusion in India is immense.

Collaboration is Key:

Government initiatives like Digital India and Jan Dhan Yojana have played a crucial role in creating a conducive environment for fintech to flourish. Continued collaboration between the government, fintech companies, and traditional financial institutions will be essential to ensure that the benefits of financial inclusion reach every corner of the country.

A Brighter Future:

As India’s fintech revolution gathers momentum, the future promises to be brighter. With increased access to financial services, rural communities will have the tools and resources to thrive. Entrepreneurs will have the capital to build their dreams, and families will have the security of insurance against life’s inevitable uncertainties. This is not just about numbers on a screen; it’s about transforming lives, fostering economic growth, and building a more inclusive and prosperous future for India.

The journey is far from over, but with each tap on a smartphone screen, each micro-loan disbursed, and each insurance policy purchased, India’s fintech revolution is etching a new chapter in the nation’s economic story. And the ending, it seems, is one of empowerment, resilience, and shared prosperity.

Mobile Wallets, UPI, and Microloans: Powering Financial Inclusion in India —

India’s financial landscape is undergoing a dynamic transformation, driven by a potent trio: mobile wallets, UPI (Unified Payments Interface), and microloans. These technological disruptors are breaking down traditional barriers, bringing millions unbanked and underbanked individuals into the fold of the formal financial system. Let’s dive deeper into their specific roles in promoting financial inclusion:

Mobile Wallets:

- Accessibility: They serve as digital substitutes for bank accounts, requiring no formal documentation or minimum balance. This opens the door for the excluded sections of society, particularly in rural areas.

- Convenience: Easy money transfers, bill payments, and even online shopping become readily available on a simple smartphone, eliminating the need for physical travel or dependence on intermediaries.

- Financial Literacy: Features like transaction history and budgeting tools promote financial awareness and responsible money management amongst users.

UPI:

- Ubiquitous Payments: By enabling instant, interbank transfers through simple phone numbers, UPI transcends geographical limitations and bank affiliations. This empowers rural communities to participate in the digital economy.

- Cost-Effectiveness: UPI leverages existing bank infrastructure, making transactions significantly cheaper compared to traditional methods. This translates to greater cost savings for users, especially low-income individuals.

- Micro-Entrepreneurship: Small businesses can accept payments seamlessly through UPI, facilitating their growth and integration into the formal economy.

Microloans:

- Financial Inclusion through Accessibility: They provide readily available credit to individuals who wouldn’t qualify for traditional loans due to lack of collateral or credit history. This empowers them to invest in small businesses, education, or healthcare needs.

- Breaking the Poverty Cycle: Access to capital enables entrepreneurship and income generation, potentially breaking the cycle of poverty and contributing to long-term economic development.

- Financial Resilience: Microloans help individuals cope with unexpected emergencies or seasonal income fluctuations, providing a safety net and fostering financial stability.

However, challenges remain:

- Digital Literacy: Bridging the digital gap and creating awareness about these tools is crucial for optimal utilization.

- Data Privacy Concerns: Robust data security measures are essential to ensure user trust and prevent misuse of personal information.

- Regulatory Framework: A balanced regulatory framework needs to be established to protect users while encouraging innovation in the fintech space.

Despite these challenges, the combined impact of mobile wallets, UPI, and microloans is undeniable. They are driving financial inclusion at an unprecedented pace, transforming lives and unlocking economic potential across India. The future holds enormous promise as these technologies evolve and cater to the specific needs of diverse communities. By addressing the existing challenges and leveraging the immense potential, India can truly achieve inclusive and sustainable economic growth, empowered by its digital financial revolution.

How Financial Inclusion Fuels Economic Thriving —

India’s journey towards financial inclusion isn’t just about numbers on a screen; it’s about weaving a richer tapestry of prosperity for the nation. By bringing millions into the formal financial system, we unlock a treasure trove of economic benefits that ripple outwards, impacting individuals, businesses, and the nation as a whole. Let’s shine a light on some of these transformative powers:

Savings: From Shadows to Sunshine

For the previously unbanked, cash was king, often hidden under mattresses or tucked away in informal schemes. This limited their ability to accumulate or protect wealth. With access to formal savings accounts, even micro-savings, individuals gain a safe haven for their hard-earned money. This fuels financial stability, builds resilience against unforeseen circumstances, and paves the way for future investments. As savings aggregate, a pool of capital gets unlocked, potentially fueling infrastructure development and social welfare programs.

Investments: From Seeds to Harvest

Financial inclusion isn’t just about saving; it’s about planting seeds for a brighter future. With access to affordable loans and micro-investments, entrepreneurs can embark on ventures, farmers can invest in better equipment and seeds, and individuals can pursue education or healthcare needs. This stimulates economic activity, creates jobs, and fosters a culture of innovation and growth. Imagine millions across India, equipped with financial tools, nurturing their dreams and contributing to a burgeoning economy.

Entrepreneurial Spirit: Uncaging the Tigers

For countless aspiring entrepreneurs, lack of access to financial credit was a brick wall blocking their paths. Microloans and crowdfunding platforms are tearing down these walls, empowering individuals to turn their ideas into reality. From small businesses blossoming in rural villages to tech startups disrupting industries, the unleashing of India’s entrepreneurial spirit holds immense potential. Financial inclusion becomes the fuel that ignites the engines of innovation and job creation, propelling the nation towards new heights of economic prowess.

Beyond Individuals: A National Transformation

The benefits of financial inclusion extend far beyond individual empowerment. As savings pool, investments flourish, and businesses thrive, the national economy receives a much-needed boost. Increased tax revenue can be channeled towards social welfare programs, healthcare initiatives, and infrastructure development, benefiting all sectors of society. A financially inclusive India, with its vibrant entrepreneurial spirit and robust domestic investments, can attract foreign capital, foster international trade, and solidify its position as a global economic powerhouse.

The road towards complete financial inclusion is still being paved, but the gains already witnessed are a testament to its transformative power. By closing the gap between the excluded and the included, we weave a tapestry of prosperity for all, where individuals flourish, businesses bloom, and a nation thrives. This is not just an economic imperative; it’s a journey towards a more equitable and vibrant India, one powered by the magic of financial inclusion.

Transforming Payment Systems: From Cash to Cosmos —

India’s vibrant bazaars, once dominated by the clinking of coins and rustling of rupee notes, are witnessing a silent revolution. Cash, the king of transactions, is being dethroned by a new wave — the wave of digital payments. This shift is not just about convenience; it’s about ushering in an era of efficiency, transparency, and security, transforming the way we interact with money and impacting various sectors from e-commerce to microbusinesses.

From Cash to Cosmos: A Paradigm Shift

For decades, cash reigned supreme in India. Transactions, big and small, were conducted with physical bills, often prone to inefficiencies, errors, and even security risks. Imagine the time wasted counting, carrying, and verifying wads of cash, the potential for human error in calculations, and the vulnerability to theft or loss.

Enter the era of digital payments. Mobile wallets, UPI transfers, contactless cards, and online payment gateways are reshaping the landscape. Transactions are now instant, accurate, and paperless. Imagine a simple tap on your phone to pay for groceries, a quick scan to settle a restaurant bill, or a seamless online purchase — all completed within seconds, with a clear digital trail for every rupee spent.

UPI: The Kingpin of Cashless Economy

At the heart of this revolution lies UPI (Unified Payments Interface), a game-changer that has democratized digital payments. This instant, interbank transfer system allows anyone with a smartphone to link their bank account to a mobile app and send or receive money using just a virtual address. No more bank account details, no more hassles — just simple, secure transfers at your fingertips.

UPI’s impact is undeniable. It has brought millions into the fold of formal finance, boosted e-commerce transactions, and empowered small businesses. Imagine kirana stores acceptingUPI payments from customers across the country, farmers receiving instant payments for their produce, or street vendors conducting cashless transactions with ease.

Ripple Effect Across Sectors:

The impact of digital payments goes beyond individual convenience. It’s creating a ripple effect across various sectors:

- E-commerce: With seamless online payments, e-commerce platforms are witnessing a boom, connecting buyers and sellers across vast distances, boosting the retail sector, and creating new job opportunities.

- Retail: From mom-and-pop shops to large chains, businesses are embracing digital payments, leading to faster checkout times, improved inventory management, and better customer experiences.

- Microbusinesses: Small vendors and entrepreneurs, who were previously cash-only, can now accept digital payments, expanding their customer base, accessing financial services, and growing their businesses.

Democratization of Credit: How Fintech is Opening Doors to Opportunity

For decades, accessing credit in India was often an arduous journey, reserved for a privileged few with established credit histories and collateral. Traditional banking models, with their rigid processes and stringent requirements, left millions, particularly individuals from underserved communities and small businesses, locked out of the financial ecosystem. But a revolution is brewing — a revolution driven by fintech lending platforms and AI-powered credit scoring, paving the way for a democratic and inclusive credit landscape.

Fintech Revolutionizing Access:

Fintech lending platforms are emerging as beacons of hope for those traditionally denied access to credit. By leveraging technology and innovative algorithms, they are bypassing the limitations of traditional models and reaching unbanked and underbanked populations. Imagine accessing a loan with just a few clicks on your phone, without mountains of paperwork or lengthy bank visits. Fintech platforms are making this a reality.

AI: The Game-Changer:

At the heart of this revolution lies AI-powered credit scoring. These algorithms analyze alternative data points, such as mobile phone usage, social media activity, and transaction history, to paint a more holistic picture of an individual’s creditworthiness. This allows fintech platforms to extend credit to those who may not have a formal credit history or traditional collateral, opening doors for the underserved and fostering financial inclusion.

Unlocking Mobility and Potential:

The impact of this democratization of credit is far-reaching. Access to loans empowers individuals to improve their lives and pursue their aspirations. Imagine a farmer investing in better equipment to increase yield, a student borrowing for higher education, or a single mother launching her own microbusiness. Fintech is unlocking financial mobility, fostering self-employment, and fueling entrepreneurial ventures across the nation.

Traditional vs. Fintech: A Tale of Two Worlds:

Compare the stark contrast between traditional and fintech models:

- Traditional: Paperwork-heavy, time-consuming processes, lengthy approval times, limited reach to rural areas.

- Fintech: Paperless, streamlined processes, instant decisions, wider reach through mobile apps, flexible loan options.

Fintech models offer greater efficiency, convenience, and flexibility, catering to the diverse needs of borrowers.

Challenges and the Future:

While the promise is immense, challenges remain. Data privacy concerns, regulatory frameworks, and ensuring responsible lending practices are crucial considerations. However, the collaborative efforts of fintech players, the government, and regulators are paving the way for a responsible and inclusive credit landscape.

As the fintech revolution gathers momentum, the future of credit in India looks bright. Imagine a world where individuals from all walks of life, regardless of background or credit history, have access to the financial tools they need to thrive. This is the future fintech is building, brick by digital brick, one loan at a time. This is the democratization of credit, where doors are flung open, and opportunity knocks for all.

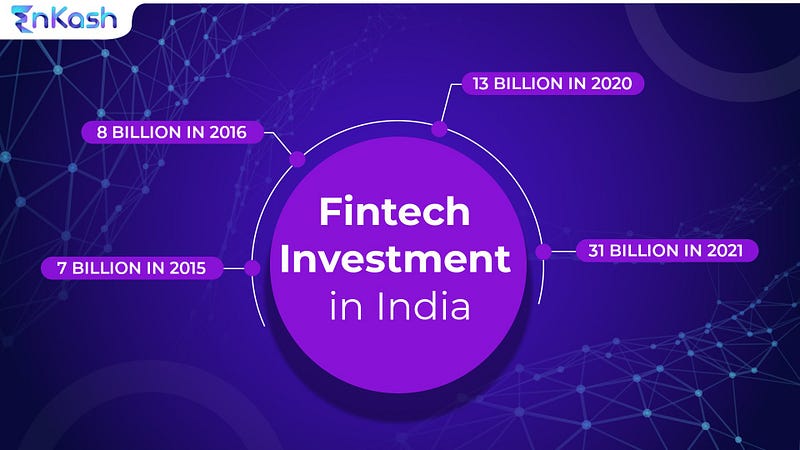

Quantifying Fintech’s Contribution to India’s GDP Growth

While isolating the exact contribution of fintech to India’s GDP is challenging due to its intertwined nature with other sectors, several estimates paint a picture of its significant impact:

- Current Contribution:

- The Indian fintech market is projected to reach $110 billion by 2024, contributing roughly 1% to India’s GDP.

- Specific segments like digital lending are expected to reach $350 billion by 2027, potentially boosting GDP by 2–3% in the coming years.

- Payments alone are projected to reach $100 trillion in transaction volume and $50 billion in revenue by 2030, further stimulating economic activity.

- Indirect Impact:

- Fintech fosters financial inclusion, bringing previously unbanked individuals and businesses into the formal economy, expanding the taxable base and overall economic activity.

- It improves efficiency and reduces costs across various sectors, leading to higher productivity and output.

- Fintech enables faster access to capital and resources for businesses, driving entrepreneurial activity and job creation.

Potential for Further Economic Advancements:

India’s thriving fintech ecosystem holds immense potential for further economic advancements, including:

- Boosting MSMEs: Streamlined lending platforms and targeted financial products can unlock the growth potential of millions of small and medium-sized enterprises, contributing significantly to India’s economic engine.

- Financial Literacy: Fintech solutions can simplify financial products and services, making them more accessible and understandable for everyone, leading to better financial decisions and wealth creation.

- Emerging Technologies: Blockchain, AI, and other emerging technologies can further revolutionize financial services, leading to increased efficiency, transparency, and innovative products.

- Rural Inclusion: By bridging the digital divide and developing localized solutions, fintech can bring financial services to rural communities, unlocking their economic potential and improving their livelihoods.

Challenges and Recommendations:

To fully unlock the potential of fintech, India needs to address certain challenges:

- Regulatory Frameworks: Continuously evolving the regulatory landscape to keep pace with innovation while ensuring consumer protection and financial stability.

- Digital Infrastructure: Expanding internet access and digital literacy, particularly in rural areas, to ensure inclusivity.

- Cybersecurity: Strengthening cybersecurity measures to build trust and confidence in the digital financial ecosystem.

- Talent Development: Investing in developing a skilled workforce equipped with the necessary skills to thrive in the rapidly evolving fintech landscape.

By overcoming these challenges and fostering a thriving fintech ecosystem, India can leverage its immense potential to achieve sustained economic growth and development, creating a more inclusive and prosperous future for all.

Increased investments, productivity gains, and improved financial management are like the holy trinity of economic development. Each plays a crucial role in a virtuous cycle that propels a nation’s economic growth and prosperity. Let’s delve into the individual impacts and their synergies:

Increased Investments:

- Boosts Capital Formation: More investments inject additional resources into the economy, providing the raw materials for businesses to expand, innovate, and create jobs. This can lead to increased production capacity, improved infrastructure, and development of new technologies.

- Creates Demand and Supply: Investments generate both employment opportunities and a demand for goods and services. This stimulates production, expands markets, and ultimately leads to higher incomes and living standards.

- Attracts Foreign Capital: High levels of investment often create a stable and attractive environment for foreign investors, bringing in additional resources and expertise that can further accelerate growth.

Productivity Gains:

- Enhances Efficiency: When workers are more productive, they generate more output with the same resources. This can lead to lower costs, competitive edge in the global market, and increased profitability for businesses.

- Drives Innovation: Productivity gains often stem from technological advancements, improved work practices, and better skills development. This continuous innovation fuels further growth and economic diversification.

- Improves Living Standards: Increased productivity ultimately translates to higher wages and increased disposable income for individuals. This boosts purchasing power, leading to a thriving consumer market and improved quality of life.

Improved Financial Management:

- Promotes Sustainable Growth: Sound fiscal policies like controlled debt levels, responsible budgeting, and efficient tax collection ensure long-term stability and prevent economic boom-and-bust cycles.

- Directs Resources Effectively: Proper financial management channels resources towards productive investments in infrastructure, education, and healthcare, laying the foundation for sustained economic progress.

- Builds Confidence and Trust: Effective financial management fosters investor confidence and creates a predictable economic environment, making the country more attractive for business and investment.

Synergies and Virtuous Cycle:

These three factors have a powerful synergistic effect. Increased investments can drive productivity gains through access to new technologies and infrastructure. Productivity gains, in turn, increase returns on investments, making them more attractive and leading to further investment. Improved financial management ensures efficient allocation of resources from these investments, maximizing their impact on productivity and furthering economic growth. This creates a virtuous cycle that fosters a dynamic and competitive economy.

It’s important to note that:

- The effectiveness of these factors depends on context and implementation. The type of investments, the focus of productivity gains, and the specific financial management strategies all play a significant role in determining the outcome.

- Distributional equality is crucial. Economic development should benefit all citizens, not just a select few. Policies need to address income inequality and ensure that everyone has the opportunity to participate in and benefit from economic growth.

Increased investments, productivity gains, and improved financial management are powerful tools for economic development. When implemented effectively and with due consideration for inclusivity, they can unlock a nation’s full potential and drive it towards a prosperous and sustainable future.

Global Impact and Challenges: India’s FinTech Journey

India’s emergence as a global fintech hub:

- Booming market: India’s fintech market is projected to reach $110 billion by 2024 and $350 billion by 2027, making it one of the fastest-growing in the world.

- Financial inclusion: Fintech is bridging the gap, bringing millions of unbanked Indians into the formal financial system, driving economic growth and development.

- Innovation hub: India boasts a vibrant ecosystem of innovative startups, offering solutions like mobile wallets, digital lending, and blockchain-based applications.

- Attract foreign investment and talent: India’s large consumer base, skilled workforce, and favorable government policies are attracting significant investments from global giants and talented fintech professionals.

Challenges for sustainable growth:

- Data security: Growing data volumes and reliance on digital channels require robust cybersecurity measures to prevent breaches and build consumer trust.

- Regulatory frameworks: Keeping pace with rapid innovation while ensuring stability and consumer protection through efficient and dynamic regulations is crucial.

- Digital literacy: Bridging the digital divide and equipping the population with basic digital skills are essential for widespread adoption and inclusive growth.

- Talent development: Investing in upskilling and reskilling initiatives to prepare the workforce for the evolving fintech landscape is key to maintaining competitiveness.

Future trends and areas of innovation:

- AI and machine learning: Personalized financial products, fraud detection, and automated risk assessment are some potential applications.

- Blockchain: Secure and transparent transactions, peer-to-peer lending, and cross-border payments are areas of exploration.

- Internet of Things (IoT): Integrating financial services with connected devices can create innovative solutions for insurance, wealth management, and micro-payments.

- Open banking: Securely sharing financial data with third-party providers can foster competition and develop new products and services.

India’s fintech journey is promising, filled with opportunities to attract global players, drive financial inclusion, and lead innovation. However, navigating the challenges of data security, regulatory frameworks, and digital literacy is crucial for ensuring sustainable and inclusive growth. Embracing future trends and actively pursuing areas of innovation will solidify India’s position as a leading force in the global fintech landscape.

Conclusion — Emphasize the impact and future potential:

India’s fintech revolution is not just a technological fad; it’s a transformative force reshaping the nation’s economic landscape. From boosting financial inclusion and driving SME growth to unlocking investment opportunities and fostering innovation, fintech is rewriting the rules of financial access and empowerment. As India embraces emerging technologies like AI and blockchain, the next wave of fintech advancements promises to further propel the country towards a more inclusive and vibrant economic future. The time is ripe for India to seize this opportunity and solidify its position as a global fintech leader, paving the way for a future where finance is accessible, efficient, and empowering for all.

Thanks.

Leave a comment