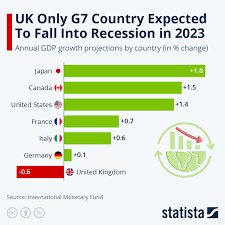

As the year 2024 unfolds, economic concerns cast a long shadow. Three economic powerhouses — China, Japan, and Britain — face the specter of recession. Individually, each nation’s economic struggles warrant attention. But collectively, the potential for a synchronized downturn raises a critical question: what are the global implications of a triple recession in 2024?

This article delves deep into the potential domino effect of these intertwined recessions. We’ll explore the unique challenges each nation faces — from China’s property market woes to Japan’s aging population and Britain’s post-Brexit uncertainties. We’ll then shift our focus to the interconnectedness of these economies, examining how trade, supply chains, and financial markets could amplify the impact of one nation’s woes on the others.

But wait, before we paint a bleak picture, let’s consider the crucial context. Is this another 2008 financial crisis brewing, or are there key differences? We’ll compare the current situation to that global recession, highlighting the distinct economic landscapes and policy responses that could shape the trajectory of 2024.

Ultimately, this article aims to provide a comprehensive understanding of the potential global impact of this triple recession. We’ll assess the risks and vulnerabilities, but also explore potential mitigation strategies and sources of resilience. By the end, you’ll have a clearer picture of what’s at stake and how prepared the world might be to weather this potential economic storm.

So, buckle up as we embark on this exploration of the interconnected world economy and the challenges — and perhaps opportunities — that lie ahead in 2024.

Individual Country Analysis: In order to understand how China, Japan and Britain’s economy will affect world economy we need to consider the countrywide analysis of recession and this can be shown by following analysis —

China:

Potential Recession:

- Real Estate Bubble: China’s booming property market faces overvaluation concerns, raising fears of a potential burst that could trigger a financial crisis. Excess debt in the sector further amplifies the risk.

- Demographic Decline: China’s population is aging rapidly, leading to a shrinking workforce and declining domestic demand, impacting economic growth potential.

- COVID-19 Lockdowns: Stringent lockdowns disrupt supply chains, hinder economic activity, and dampen consumer confidence. While the policy has relaxed, uncertainty remains.

Global Trade & Manufacturing:

- Dominant Player: China is the world’s largest exporter of goods, playing a crucial role in global supply chains. Its manufacturing prowess makes it a key player in various industries.

- Trade Tensions: Trade disputes with the US and other countries create uncertainties, impacting export-oriented businesses and raising costs for consumers globally.

Japan:

Long-Standing Stagnation:

- “Lost Decades”: Japan has experienced sluggish economic growth since the 1990s asset bubble burst, dubbed the “Lost Decades.” Deflationary pressures and structural rigidities have hampered recovery.

- Aging Population: Similar to China, Japan’s aging population shrinks the workforce and reduces consumption, further weighing on growth.

Export Reliance & China Dependence:

- Export-Driven: Japan heavily relies on exports, making it vulnerable to global economic fluctuations and trade disruptions.

- China Dependence: China is Japan’s largest trading partner, increasing vulnerability to economic slowdowns in China.

Britain:

Brexit Impact:

- Trading Challenges: Brexit introduced new trade barriers, impacting businesses and increasing costs, dampening economic activity.

- Uncertainties: Ongoing negotiations and regulatory changes create uncertainty for businesses, hindering investment and growth.

Rising Inflation & Political Uncertainty:

- High Inflation: The UK faces higher inflation than other developed economies, squeezing household budgets and eroding consumer confidence.

- Political Instability: Recent political changes and potential future uncertainties can further weaken investor confidence and hinder economic decision-making.

Financial Hub & Global Trade:

- Financial Center: London remains a major global financial center, but competition from other hubs like Singapore is increasing.

- Trade Significance: The UK maintains its importance in global trade, despite Brexit challenges, especially in services and certain goods.

Interconnectedness and Domino Effect of Recessions:

The potential recessions in China, Japan, and Britain could trigger a domino effect through interconnected trade, supply chains, and financial markets, amplifying the individual country’s problems and creating a global economic downturn. Here’s how:

Trade & Supply Chains:

- China Slowdown: A decline in Chinese demand for imports would negatively impact exports from Japan and Britain, particularly in sectors like manufacturing and raw materials. This could lead to job losses, production cuts, and further economic slowdown in these countries.

- Supply Chain Disruptions: If any of these countries experience production disruptions due to recessions, it could create bottlenecks and shortages in global supply chains, impacting businesses worldwide and potentially raising prices for consumers.

Financial Markets:

- Market Contagion: A recession in any of these major economies could trigger panic selling in global financial markets, leading to asset price declines and tighter credit conditions. This could further dampen economic activity across the globe.

- Currency Devaluations: Countries might resort to competitive currency devaluations to boost exports, leading to trade wars and protectionist measures, hindering global trade and economic cooperation.

Potential Trade Conflicts & Protectionism:

- Increased Protectionism: Governments facing recessionary pressures might implement protectionist measures like tariffs or quotas to shield domestic industries, leading to trade conflicts and reduced global trade volume.

- Trade Bloc Tensions: Existing trade tensions between major economies could escalate as countries prioritize domestic interests, potentially fracturing trade blocs and hindering global economic integration.

Domino Effect Examples:

- China’s property market crash: This could trigger a financial crisis in China, impacting global markets and reducing Chinese demand for imports, hurting Japan and Britain’s exports.

- Japan’s deflation: Deflationary pressures in Japan could lead to lower wages and reduced domestic demand, further impacting its trading partners like China and Britain.

- Brexit’s long-term impact: If the UK struggles to adapt to post-Brexit realities, its economic slowdown could ripple through Europe and its trading partners, including China and Japan.

The interconnectedness of the global economy means that recessions in major economies like China, Japan, and Britain can have cascading effects on each other and the world. Trade disruptions, financial market panic, and protectionist policies can amplify the initial problems, creating a complex and challenging economic environment.

It is important to remember that this is a hypothetical scenario, and the actual impact of any recession will depend on various factors, including the severity of the downturn, policy responses, and global economic conditions. However, understanding the potential interconnectedness and domino effects can help us prepare for and mitigate the risks associated with economic downturns.

Comparing Potential Recessions to the 2008 Financial Crisis:

While concerns surround potential recessions in China, Japan, and Britain, comparing them to the 2008 financial crisis reveals critical differences:

Key Differences:

- Financial System: Post-2008 regulations have strengthened banks’ capital requirements and risk management, making them less susceptible to systemic collapse.

- Debt Levels: While debt remains high in some countries, it’s not at systemic levels seen in 2008, potentially limiting the cascading effect of defaults.

- Central Bank Preparedness: Central banks now have more experience and tools to address crises, like quantitative easing and targeted asset purchases.

Potential Resilience:

These differences suggest the global economy might be better equipped to handle downturns compared to 2008, but challenges remain:

- Unforeseen Events: New shocks like geopolitical tensions or climate disasters could still trigger widespread instability.

- Emerging Market Vulnerabilities: Some emerging economies remain susceptible due to high debts and dependence on external financing.

- Income Inequality: Unequal distribution of wealth can amplify recessions’ impact on vulnerable populations, potentially leading to social unrest.

Uncertainties and Nuances:

- China’s Real Estate Bubble: While less systemic than 2008’s subprime crisis, its bursting could still have significant global ramifications.

- Geopolitical Tensions: Trade wars, sanctions, and regional conflicts can significantly disrupt trade and investment, exacerbating economic downturns.

- Unconventional Monetary Policy: The effectiveness of central bank tools after years of unconventional policies like quantitative easing remains under debate.

While the global economy might be more resilient than in 2008, potential recessions in major economies still pose significant risks. Careful monitoring, international cooperation, and targeted policy responses are crucial to mitigate the impact and foster inclusive recovery.

Global Impact of a Triple Recession:

A simultaneous recession in China, Japan, and Britain, often referred to as a “triple recession,” could trigger significant ripple effects across the global economy. Here’s how it could impact various aspects:

Global Economic Growth:

- Synchronized Slowdown: If all three major economies experience recessions, it could lead to a synchronized global slowdown, reducing global GDP growth significantly.

- Reduced Trade: Decreased demand from these large economies could hamper global trade, impacting export-oriented businesses worldwide.

- Investment Decline: Uncertainty and risk aversion might lead to a decline in global investment, further dampening economic activity.

Commodity Prices:

- Demand-Driven Decline: With reduced demand from major consumers like China, prices of commodities like oil, metals, and agricultural products could fall significantly.

- Impact on Producers: This could negatively impact resource-rich emerging markets and countries heavily reliant on commodity exports.

- Geopolitical Tensions: Price fluctuations and competition for declining demand could exacerbate existing geopolitical tensions among resource-producing nations.

Financial Markets:

- Volatility and Risk Aversion: Economic slowdown and uncertainty could lead to increased volatility in global financial markets, with investors shifting towards safer assets and risk-averse behavior.

- Emerging Market Capital Flight: Investors might withdraw capital from emerging markets perceived as riskier, potentially triggering currency depreciation and financial instability.

- Central Bank Response: Central banks might need to implement coordinated policies to address market volatility and ensure financial stability.

Emerging Markets:

- Vulnerability: Due to their reliance on foreign capital and commodity exports, emerging markets could be particularly vulnerable to the impacts of a triple recession.

- Debt Vulnerabilities: Many emerging markets are already struggling with high debt levels, and a global economic slowdown could make it more difficult to service their debts.

- Social Unrest: Economic hardship and rising unemployment could lead to social unrest and political instability in some emerging markets.

Additional Considerations:

- Policy Response: Coordinated and effective policy responses from major economies and international institutions can significantly mitigate the global impact of a triple recession.

- Geopolitical Context: The severity of the impact will also depend on the broader geopolitical context, including ongoing trade wars and regional conflicts.

- Technological Innovation: Technological advancements and investments in green technologies could offer opportunities for mitigating the downturn and fostering sustainable recovery.

A triple recession in China, Japan, and Britain would undoubtedly have significant global ramifications. While the global economy might be better equipped than in 2008, coordinated international efforts and targeted policies are crucial to minimize the impact and support a sustainable recovery. Remember, this analysis is based on hypothetical scenarios, and the actual impact will depend on various evolving factors.

Mitigation Strategies and Sources of Resilience:

While the prospect of a “triple recession” is concerning, several strategies and sources of resilience can offer hope for minimizing its impact:

Government & Central Bank Responses:

- Fiscal Stimulus: Targeted government spending on infrastructure, social programs, and green initiatives can boost domestic demand and create jobs.

- Monetary Policy: Central banks can utilize tools like interest rate cuts and quantitative easing to inject liquidity into the economy and encourage borrowing and investment.

- Trade Cooperation: International agreements to reduce trade barriers and promote free trade can help mitigate the decline in global trade.

- Financial Regulation: Maintaining and strengthening financial regulations can prevent systemic risks and ensure financial stability.

- Social Safety Nets: Expanding social safety nets like unemployment benefits can protect vulnerable populations and reduce social unrest during downturns.

Sources of Resilience:

- Strong Domestic Demand: Some countries with strong domestic demand, like the US, could offer some counterbalance to the declines in China, Japan, and Britain.

- Technological Advancements: Continued investments in technology and innovation can drive productivity growth and create new industries and jobs.

- Regional Diversification: Businesses and countries with diversified trade relationships and less reliance on the affected economies might be less impacted.

- Green Transition: Investments in renewable energy and sustainable infrastructure can create new opportunities and mitigate the impact of climate change.

- International Cooperation: Coordinated efforts by governments and international institutions can offer financial assistance, share resources, and provide guidance for recovery.

Additional Considerations:

- Policy effectiveness: The effectiveness of these strategies will depend on their design, implementation, and coordination across different countries and sectors.

- Long-term impact: While these measures can alleviate the immediate impact of recessions, addressing structural issues like inequality and climate change is crucial for long-term resilience.

- Political and social context: Political stability and social cohesion are essential for effective policy implementation and mitigating social unrest during economic downturns.

The potential “triple recession” presents significant challenges, but proactive policy responses and existing sources of resilience within the global economy offer hope for mitigating its impact and fostering a sustainable recovery. Remember, this is a complex scenario with various uncertainties, and ongoing monitoring and adaptation of strategies will be crucial in navigating the evolving situation.

Conclusion — The possibility of simultaneous recessions in China, Japan, and Britain in 2024 paints a sobering picture, with potential ramifications rippling across the global landscape. From synchronized economic slowdown to financial market volatility and emerging market vulnerabilities, the domino effect could be significant.

However, amidst the uncertainties, glimmers of hope shine through. Stronger financial regulations, international cooperation, and sources of resilience within individual economies offer opportunities to mitigate the impact and foster recovery. Targeted policy responses like fiscal stimulus, monetary easing, and trade cooperation can act as buffers, while strong domestic demand in some countries and ongoing advancements in technology provide counterbalancing forces.

Ultimately, the severity of the global impact will hinge on a complex interplay of factors. Coordinated international efforts, proactive policy responses, and continued investments in long-term resilience will be crucial in navigating this uncertain terrain. While challenges lie ahead, by learning from past crises, embracing the potential of innovation, and prioritizing international cooperation, we can navigate this potential triple recession and build a more sustainable and equitable global economy.

Thanks.

Leave a comment