Rising Rates, Fragile Markets: The Next Big Blowup for the Financial System?

For over a decade, historically low interest rates have fueled a seemingly endless boom in financial markets. Asset prices have soared, from stocks and bonds to real estate and cryptocurrencies. This era of easy money, however, may be nearing its end. Central banks around the world, facing persistent inflation, are signaling a shift towards tighter monetary policy, with interest rate hikes on the horizon. This seemingly innocuous change has the potential to trigger a seismic shift in the financial landscape, exposing vulnerabilities that have festered during the years of easy credit.

This article delves into the potential consequences of rising interest rates on a system built on the foundation of low borrowing costs. We’ll explore how higher rates could impact various asset classes, from equities sensitive to future earnings potential to heavily indebted corporations facing refinancing challenges. We’ll also examine the potential domino effect on fragile market segments, scrutinizing potential flashpoints like overvalued housing markets or highly leveraged investment vehicles.

The question remains: will rising rates trigger a controlled slowdown or a full-blown financial crisis? By analyzing historical precedents, assessing current market vulnerabilities, and exploring potential policy responses, this article aims to equip readers with a deeper understanding of the potential risks and opportunities presented by this critical juncture in the global financial system.

Impact of Rising Rates on Asset Classes:

Equities:

Rising interest rates can have a two-pronged effect on stock valuations, especially for growth stocks:

- Discounted Future Cash Flows: Companies are valued based on the present value of their future earnings potential. When interest rates rise, the discount rate used to calculate this present value also increases. This means the current value of a company’s future earnings (a key driver for growth stocks) gets discounted more heavily, potentially leading to lower stock prices.

- Investor Sentiment: Higher interest rates can make borrowing more expensive for companies, potentially hindering their growth plans. Additionally, investors may be drawn towards the higher yields offered by bonds, leading to a shift away from stocks and putting downward pressure on equity prices.

This environment may favor value stocks. These companies typically have more established business models, generate consistent cash flows, and offer dividends. Value stocks are generally less sensitive to interest rate fluctuations as their current profitability carries more weight compared to future growth potential.

Bonds:

The relationship between interest rates and bond prices is inverse. When interest rates rise, the value of existing bonds with lower coupon rates (fixed interest payments) decreases. This is because investors can now buy new bonds with higher yields, making the older bonds with lower yields less attractive.

This dynamic can lead to losses in bond portfolios, especially for fixed-income investors who bought bonds when interest rates were much lower. These bonds may now trade below their face value to reflect the prevailing higher interest rates.

Real Estate:

Rising interest rates directly impact mortgage affordability. Higher borrowing costs make it more expensive to buy a house, potentially leading to a decrease in demand and a slowdown in the housing market. This is particularly relevant in markets that have seen significant price hikes in recent years, as rising rates could price out some potential buyers and cool down the market.

However, the impact might not be uniform across all segments. Luxury properties might be more susceptible to a slowdown, while affordable housing could see continued demand due to underlying needs.

Cryptocurrencies:

Cryptocurrencies are considered riskier assets compared to traditional investments like stocks and bonds. When interest rates rise, investors generally become more risk-averse. This could dampen the enthusiasm for cryptocurrencies, leading to price volatility as investors move their capital towards safer havens like bonds or cash.

The lack of inherent value or cash flow generation in most cryptocurrencies makes them even more sensitive to broader market sentiment shifts triggered by rising interest rates.

Rising Interest Rates and the Corporate Debt Challenge: The era of historically low-interest rates witnessed a significant increase in corporate debt. Companies took advantage of cheap borrowing to finance expansion, acquisitions, share buybacks, and stock dividends. While this fueled economic growth, it also created a situation where many corporations are now heavily leveraged.

Rising interest rates pose a significant challenge to this corporate debt landscape:

- Increased Borrowing Costs: As interest rates climb, the cost of servicing existing debt becomes more expensive. Companies will have to dedicate a larger portion of their cash flow to interest payments, potentially impacting profitability and hindering future investments.

- Refinancing Challenges: Many corporations issued bonds with fixed interest rates during the low-rate environment. When these bonds mature, refinancing them at the prevailing higher rates can significantly increase borrowing costs. Companies with limited cash flow or weakening financial performance may struggle to refinance, potentially leading to defaults.

These factors can create a domino effect:

- Profitability Squeeze: Higher interest expenses eat into corporate profits, limiting their ability to invest in growth initiatives, research and development, or hiring. This can hinder long-term competitiveness and further strain financial health.

- Default Risk: Companies struggling with high debt burdens and rising borrowing costs may eventually default on their loans. This can lead to bankruptcies, job losses, and disruptions in the supply chain.

Contagion Risk: The problems in one sector can quickly spread to others, creating a wider financial crisis. Here’s how:

- Interconnectedness: Many corporations have complex financial relationships. A default in one sector could trigger a ripple effect, impacting companies in its supply chain or those that have lent money to the struggling firm.

- Investor Confidence: Defaults and bankruptcies can erode investor confidence in the overall market. This can lead to a sell-off across different asset classes, further exacerbating financial instability.

Mitigating the Risks:

- Debt Management: Corporations with high debt levels need to proactively manage their debt by extending maturities, restructuring loans, and prioritizing debt repayment.

- Building Cash Buffers: Maintaining a healthy cash reserve can help companies weather temporary setbacks and provide a cushion when interest rates rise.

- Transparency: Clear communication with investors and lenders regarding debt management strategies can build trust and stability during periods of rising interest rates.

By acknowledging the challenges and taking proactive steps, corporations can navigate the rising interest rate environment and maintain financial stability.

Market Vulnerabilities Exposed by Rising Interest Rates: Rising interest rates can act as a stress test, exposing underlying vulnerabilities in the financial system. Here are some key areas of concern:

Flashpoints:

- Overvalued Assets: If certain asset classes, like stocks or real estate, have become significantly overvalued during the low-interest-rate period, a rise in rates can trigger a sharp correction. As the cost of capital increases, investors may re-evaluate valuations, leading to a potential market crash.

- Highly Leveraged Investment Vehicles: Hedge funds, private equity firms, and other investment vehicles that rely heavily on borrowed money to amplify returns become more vulnerable when interest rates rise. Higher borrowing costs can squeeze their margins and potentially lead to defaults if they are unable to meet their debt obligations.

- Interconnectedness: The modern financial system is highly interconnected. Problems in one sector, like a major bank default, can quickly ripple through the entire system as institutions have exposure to each other through loans, investments, and derivatives. This interconnectedness can amplify the impact of isolated events, leading to a wider financial crisis.

Feedback Loops:

Rising interest rates can create a vicious cycle known as a feedback loop:

- Market Decline: As interest rates rise, asset prices across different markets (stocks, bonds, real estate) may start to decline. This decline can trigger:

- Margin Calls: Investors who borrowed money to buy assets may face margin calls from lenders if the value of their holdings falls below a certain threshold. This forces them to sell assets to meet the margin call, further depressing prices.

- Risk Aversion: Seeing market declines, investors may become more risk-averse and sell their assets to prevent further losses. This selling pressure can accelerate the downward spiral in prices.

This self-reinforcing mechanism can lead to a significant market correction, exacerbating the initial decline and potentially leading to financial instability.

- Central Bank Actions: The effectiveness of central banks in managing rising interest rates is crucial. If they raise rates too aggressively, it can trigger a recession. Conversely, if they raise rates too slowly, inflation could spiral out of control.

- Geopolitical Events: Global events like wars, political instability, or trade disruptions can add further pressure to the financial system during periods of rising interest rates.

By understanding these vulnerabilities and potential feedback loops, policymakers, financial institutions, and investors can take steps to mitigate risks and promote financial stability during periods of rising interest rates.

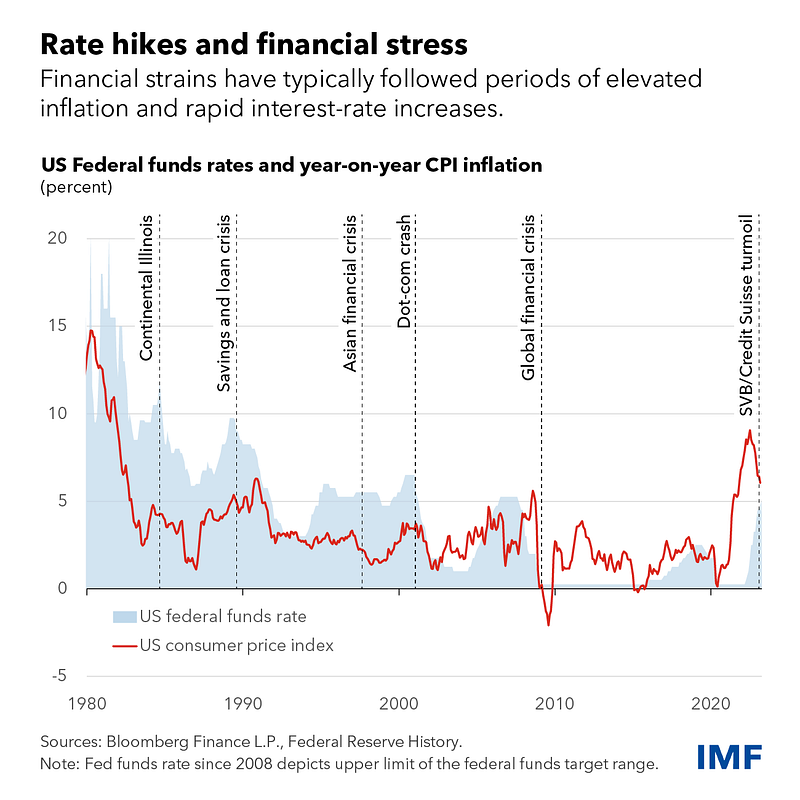

Historical Precedents: Rising Rates and Financial Crises — History offers valuable lessons on how rising interest rates can trigger financial crises. Let’s explore a past example and analyze its relevance to the present:

- Savings & Loan Crisis (1980s): In the United States during the 1980s, deregulation coupled with low-interest rates led Savings & Loan institutions (S&Ls) to aggressively invest in riskier, high-yield loans. When interest rates rose sharply in the early 1980s, many of these loans went bad, causing widespread defaults. The crisis ultimately cost US taxpayers billions of dollars to resolve.

Insights from the Past:

The S&L crisis offers valuable insights into the potential dangers of rising interest rates:

- Moral Hazard: When interest rates are low, institutions may engage in riskier behavior, assuming that low rates will persist. When rates rise, these risks can come to fruition, leading to financial instability.

- Asset Bubbles: Low-interest rates can fuel asset bubbles in specific sectors like real estate. Rising rates can then burst these bubbles, causing significant losses for investors and institutions heavily exposed to those assets.

The Current Landscape:

While the S&L crisis provides valuable lessons, it’s important to acknowledge the differences in the present financial system:

- Regulation: The financial system has undergone significant regulatory reforms since the S&Ls crisis. These reforms aim to make institutions more resilient to economic shocks.

- Globalized Markets: The financial system is now far more globalized than in the 1980s. This interconnectedness can amplify both positive and negative trends, making it harder to predict the precise impact of rising interest rates.

Learning from History:

By studying past financial crises, we can:

- Identify Potential Vulnerabilities: Understanding how past crises unfolded can help us identify similar vulnerabilities in the current system and take steps to mitigate them.

- Develop Robust Policies: Policymakers can learn from past mistakes and craft regulations that promote financial stability while allowing for a healthy flow of credit.

- Promote Market Discipline: Understanding the risks associated with low-interest rates can encourage market participants to act more responsibly and avoid excessive leverage.

However, it’s crucial to remember that history doesn’t always repeat itself perfectly. The current financial system is complex and constantly evolving, which means that the impact of rising interest rates this time around could be different from past episodes.

Policy Response to Rising Interest Rates: Managing the Transition — Central banks and governments play a critical role in navigating the transition to higher interest rates and mitigating potential financial risks. Here’s a breakdown of their potential actions:

Central Banks:

- Gradual Rate Hikes: Central banks can raise interest rates gradually to minimize the disruptive impact on the economy and financial markets. This allows businesses and consumers time to adjust to the higher borrowing costs.

- Clear Communication: Clearly communicating the rationale behind rate hikes and the expected pace of future adjustments can manage market expectations and maintain investor confidence.

- Liquidity Management: Central banks can use liquidity tools to ensure smooth functioning of the financial system. This might involve injecting additional liquidity if markets become overly stressed during the rate hike cycle.

Government Policies and Regulations:

- Stress Testing: Regulatory bodies can stress test financial institutions to assess their resilience to rising interest rates. This helps identify potential vulnerabilities and prompt institutions to take corrective measures.

- Capital Adequacy: Raising capital adequacy requirements for banks can ensure they have sufficient buffers to absorb potential losses if borrowers default on their loans due to higher interest rates.

- Targeted Measures: Governments might consider targeted measures to support specific sectors vulnerable to rising rates, such as providing loan guarantees for small businesses.

Balancing Act:

The key challenge lies in striking a balance between:

- Controlling Inflation: Central banks need to raise rates sufficiently to control inflation and maintain price stability.

- Maintaining Economic Growth: Excessive rate hikes can stifle economic activity and potentially lead to recession.

International Coordination:

Given the interconnectedness of global financial markets, international coordination between central banks is crucial. This helps to ensure that rate hikes by one country don’t trigger unintended consequences in another.

Transparency and Communication:

Both central banks and governments need to be transparent in their communication with the public and financial markets. This transparency builds trust and helps manage expectations during a period of economic uncertainty.

A well-coordinated policy response from central banks and governments is essential to navigate the transition to higher interest rates. By taking proactive measures and fostering open communication, policymakers can mitigate financial risks and promote a stable economic environment.

Conclusion — Rising interest rates present a complex challenge for the financial system. While necessary to combat inflation, they can expose vulnerabilities and trigger market corrections. By acknowledging the potential risks, learning from historical precedents, and implementing a coordinated policy response, policymakers and market participants can work together to navigate this period of economic transition.

This doesn’t necessarily mean a “big blowup” is inevitable. Prudent risk management, clear communication, and a focus on financial stability can help us weather the rising rate environment and foster a more sustainable economic future.

Thanks.

Leave a comment