Monetarism vs. Keynesianism: Rethinking Discretionary Policy and Aggregate Demand Management in the Modern Era

The economic landscape of the 21st century presents a complex challenge for policymakers. The Great Recession shattered some of the core tenets of traditional economic thought, prompting a reevaluation of how best to manage economic fluctuations. This article explains the ongoing debate between two dominant schools of macroeconomic thought that is, Monetarism and Keynesianism.

Monetarism, with its emphasis on a rules-based approach to controlling the money supply, has long been a cornerstone of economic policy. However, the effectiveness of this rigid approach in a world of ever-evolving financial markets and global interconnectedness is increasingly questioned.

Keynesianism, on the other hand, advocates for a more active role for government intervention in managing aggregate demand. By influencing both fiscal and monetary policy, Keynesians argue, policymakers can mitigate the negative effects of economic downturns and promote sustained growth.

This article examines the strengths and weaknesses of both Monetarism and Keynesianism, particularly in light of the modern economic environment. We will explore the limitations of a purely rules-based approach to monetary policy and the potential benefits of a more discretionary approach that can adapt to changing economic circumstances. Furthermore, we will analyze the role of fiscal policy in conjunction with monetary policy, as advocated by Keynesian economics.

Ultimately, the goal is to shed light on the ongoing debate and explore the most effective strategies for navigating the complexities of the modern economy. We will consider whether a rethinking of both Monetarism and Keynesianism is necessary, or if a hybrid approach that incorporates elements of both schools of thought might be the most prudent path forward.

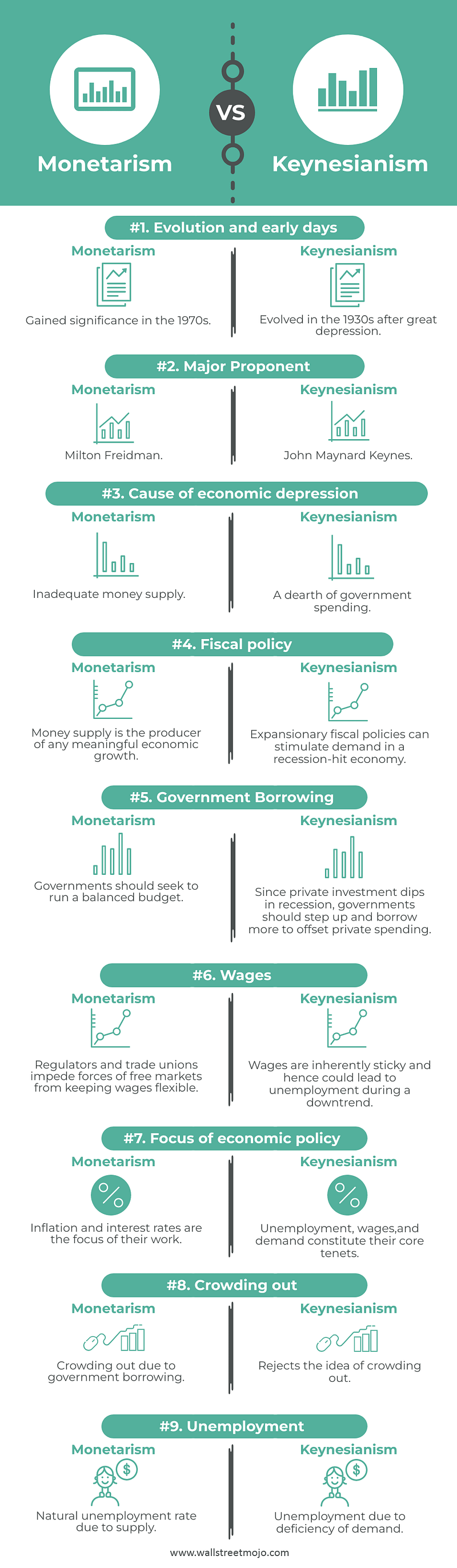

Monetarism’s Limitations: A Closer Look — Monetarism, championed by economist Milton Friedman, has been a dominant economic theory for decades. However, its emphasis on controlling the money supply to manage inflation has some shortcomings in today’s intricate financial landscape. Here’s a detailed breakdown of these limitations:

1. Overly Simplistic View of the Money Supply:

- Monetarist Assumption: A core principle of monetarism is the quantity theory of money, which posits a direct relationship between the money supply (amount of currency and credit in circulation) and inflation. Simply put, more money chasing the same amount of goods and services leads to price hikes (inflation).

- The Reality of Modern Finance: This theory, however, overlooks the complexities of the modern financial system. Factors like:

- Velocity of Money: How quickly money changes hands can significantly impact inflation. Monetarism often assumes a stable velocity, which isn’t always the case. During economic downturns, people might hoard cash, reducing velocity and weakening the link between money supply and inflation.

- Credit Instruments: The rise of various credit instruments like bonds and derivatives creates new sources of money supply beyond traditional currency. These can influence inflation independently of the central bank’s control.

- Asset Bubbles: Inflated asset prices (stock market bubbles) can create a wealth effect, where people feel richer and spend more, even without an increase in the money supply, pushing inflation upwards.

2. Limited Effectiveness in Addressing Recessions:

- Monetarist Response: Monetarism advocates for a gradual increase in the money supply to promote economic growth and prevent deflation. However, this approach might be slow-acting.

- Recessionary Challenges: During a sudden economic downturn, businesses might hesitate to invest, and consumers might tighten their belts. Simply increasing the money supply might not translate into immediate growth. The time it takes for this policy to take effect can lead to prolonged recessions.

- Alternative Approaches: Keynesian economics, for instance, argues for government spending to stimulate demand during recessions, offering a potentially faster response.

3. Inflexibility in a Globalized Economy:

- Monetary Policy and National Borders: Monetarism assumes a nation’s central bank can control its economy primarily through domestic monetary policy.

- The Interconnected World: In today’s globalized world, capital flows freely across borders. Interest rates set by one country can influence investment decisions and currency exchange rates in others. This can limit the effectiveness of a single nation’s monetary policy in influencing its own economy.

While monetarism provides valuable insights into managing inflation, its limitations in a complex financial environment and its potentially slow response to recessions necessitate a more nuanced approach to economic policy. Modern central banks often combine elements of monetarism with other economic theories to achieve their goals.

Keynesianism’s Considerations: Keynesian economics, developed by John Maynard Keynes, emphasizes the role of government intervention in managing economic fluctuations. While it offers valuable tools for promoting economic stability, it’s crucial to consider its strengths and potential drawbacks.

1. Importance of Fiscal Policy:

- Beyond Monetary Policy: Unlike monetarism, which focuses primarily on controlling the money supply, Keynesianism advocates for using both fiscal policy (government spending and taxation) and monetary policy to manage aggregate demand (total spending in the economy).

- A Two-Pronged Approach: This allows for a more comprehensive approach to economic management. For instance:

- Stimulating Demand: During recessions, the government can increase spending on infrastructure projects or social programs, injecting money directly into the economy and boosting demand for goods and services. This can help counter falling private sector investment and consumption.

- Curbing Inflation: Conversely, during periods of high inflation, the government can raise taxes, reducing disposable income and dampening demand.

2. Timely Government Intervention:

- Proactive Approach: A core principle of Keynesianism is the need for proactive government intervention during economic downturns. This aims to prevent a negative feedback loop where falling demand leads to business closures, job losses, and further decline in demand.

- Automatic Stabilizers: Keynesian theory supports the use of automatic stabilizers, which are built-in features of the tax and spending system that automatically adjust in response to economic conditions. For example, unemployment benefits rise during recessions, providing support to individuals and maintaining some level of demand.

3. Potential for Government Overreach:

- The Efficiency Question: Excessive government intervention can lead to inefficiencies in resource allocation. Government projects might not be as efficient as private sector initiatives, and some argue that government spending can create a disincentive for private investment.

- Distortionary Effects: Tax policies aimed at stimulating demand or curbing inflation can have unintended consequences. High taxes can discourage investment and entrepreneurship, while distortionary spending can lead to projects that wouldn’t be viable without government support.

Finding the Right Balance:

Keynesianism offers valuable tools for promoting economic stability, particularly during recessions. However, it’s important to acknowledge the potential for government overreach and ensure policies are designed effectively. The optimal approach likely involves a combination of fiscal and monetary policy, implemented with a clear understanding of potential trade-offs.

The Need for Rethinking: Reevaluating Economic Policy Frameworks — The Great Recession of 2008 and the subsequent slow recovery exposed limitations in both monetarist and Keynesian economic models. This has led to a growing call for reevaluation and adaptation of traditional economic policy frameworks. Here’s a closer look at the factors driving this need for change:

1. The Great Recession’s Impact:

- A Wake-Up Call: Both monetarism and Keynesianism struggled to predict the severity of the 2008 financial crisis and design effective responses.

- Monetarist Shortcomings: The crisis highlighted the limitations of focusing solely on the money supply. Unconventional factors like asset bubbles and deregulation of financial markets played a significant role, which monetarism didn’t adequately address.

- Keynesian Challenges: While Keynesian stimulus helped prevent a deeper depression, its effectiveness in fostering a robust recovery was debated. The high level of debt accumulated by governments raised concerns about long-term sustainability.

2. Adaptability in a Dynamic Economy:

- The Evolving Landscape: Financial markets are constantly innovating, with new financial instruments and complex interactions emerging. Economic policy frameworks need to be flexible enough to adapt to these changes.

- Beyond Traditional Tools: Monetarist and Keynesian tools, designed for a simpler economic environment, might not be sufficient to address the complexities of the modern financial system.

- The Need for New Approaches: Policymakers need to consider new tools and frameworks that can address issues like:

- Shadow Banking: The growth of non-bank financial institutions that operate outside traditional regulations.

- Financial Interconnectedness: The increased interconnectedness of global financial markets, where events in one region can quickly cascade to others.

The COVID-19 Pandemic and Russia-Ukraine War: A Double Whammy for Economic Policy

The global economy has been buffeted by two major crises in recent years: the COVID-19 pandemic and the Russia-Ukraine war. These events have significantly impacted economic policymaking, forcing governments and central banks to adapt their strategies in a rapidly changing environment. Let’s delve deeper into the specific challenges these crises pose:

1. COVID-19’s Economic Fallout:

- Supply Chain Disruptions: Lockdowns and travel restrictions disrupted global supply chains, leading to shortages of essential goods and raw materials. This pushed prices higher and created bottlenecks in production.

- Labor Market Turmoil: The pandemic caused widespread job losses and business closures, leading to unemployment and a decline in aggregate demand.

- Shifting Consumer Behavior: Consumer spending patterns changed dramatically, with a rise in demand for online shopping and home goods, while demand for travel and leisure services plummeted.

Policy Responses:

- Stimulus Packages: Governments across the globe implemented massive fiscal stimulus packages to support businesses and individuals during lockdowns. This helped prevent a deeper economic downturn but also led to increased government debt.

- Quantitative Easing: Central banks employed quantitative easing (QE) by purchasing government bonds, injecting liquidity into the financial system, and keeping interest rates low. This aimed to encourage borrowing and investment.

2. The Russia-Ukraine War’s Economic Shockwaves:

- Energy Crisis: The war significantly disrupted global energy markets, as Russia is a major exporter of oil and natural gas. This led to a spike in energy prices, further fueling inflation.

- Food Security Concerns: Ukraine is a major exporter of wheat and other agricultural products. The war disrupted agricultural production and exports, exacerbating food insecurity, particularly in developing countries.

- Global Economic Uncertainty: The war heightened global economic uncertainty, leading businesses to delay investment and consumers to tighten their spending.

Policy Challenges:

- Taming Inflation: The combined effect of supply chain disruptions and the energy crisis has pushed inflation to multi-decade highs in many countries. Central banks are now facing the difficult task of raising interest rates to combat inflation without triggering a recession.

- Balancing Growth and Stability: Policymakers need to find a delicate balance between supporting economic growth and curbing inflation. Tightening monetary policy can slow down growth, while excessive stimulus can further exacerbate inflation.

- Addressing Global Food Insecurity: The war in Ukraine has highlighted the vulnerability of global food supply chains. Policymakers need to find ways to ensure food security for vulnerable populations, potentially through increased agricultural production and trade diversification.

The COVID-19 pandemic and the Russia-Ukraine war have exposed the fragility of the global economy and the interconnectedness of global supply chains. Economic policymakers are facing a challenging environment characterized by high inflation, potential recessions, and new geopolitical uncertainties. They will need to adapt their strategies, potentially through:

- International Cooperation: Increased cooperation among countries is crucial to address global challenges like food insecurity and climate change.

- Investing in Resilience: Building more resilient supply chains and fostering domestic production of essential goods can help mitigate the impact of future disruptions.

- Long-term Sustainability: Policymakers need to consider long-term economic sustainability alongside short-term crisis response. This might involve promoting renewable energy sources and fostering innovation to address climate change.

The coming years will likely see continued adjustments to economic policies as the world grapples with the ongoing effects of these crises. Adaptability, innovation, and international cooperation will be key to navigating these challenging times.

3. The Rise of New Economic Challenges:

- Beyond GDP: Traditional economic models focus primarily on economic growth, measured by Gross Domestic Product (GDP). However, the 21st century presents new challenges that need to be factored into economic policy:

- Income Inequality: The widening gap between rich and poor can lead to social unrest and hinder long-term economic growth.

- Environmental Sustainability: Climate change and resource depletion necessitate policies that promote sustainable economic development.

- Technological Disruptions: Automation and artificial intelligence have the potential to disrupt labor markets and require proactive policies to address potential unemployment and income inequality issues.

Rethinking Economic Policy:

The Great Recession and the emergence of new economic challenges necessitate a reevaluation of traditional economic policy frameworks. Policymakers need to consider a wider range of factors, embrace adaptability, and potentially develop new tools to address the complexities of the 21st century economy. This might involve incorporating insights from behavioral economics, ecological economics, and other emerging fields into economic policy design.

The New Economic Landscape — The COVID-19 pandemic and the Russia-Ukraine war have highlighted the limitations of traditional economic frameworks. Here, we explore some potential solutions for policymakers to navigate this complex economic landscape:

1. Hybrid Approach: Blending Strategies —

- Beyond Monetarism or Keynesianism Alone: Neither monetarism’s sole focus on money supply nor Keynesianism’s emphasis on government intervention may be sufficient in today’s dynamic environment.

- A Strategic Blend: A hybrid approach could involve:

- Monetary Policy Framework: Setting long-term inflation targets and utilizing monetary instruments like interest rates to achieve them, drawing on principles of monetarism.

- Fiscal Policy Flexibility: Allowing for discretionary fiscal stimulus during economic downturns to support demand, drawing on Keynesian principles.

- Tailored Responses: Adapting policy responses based on the specific nature of economic challenges. For instance, the current environment calls for measures to address inflation alongside potential recessionary risks.

2. Focus on Financial Stability —

- Beyond Aggregate Demand: While managing aggregate demand through monetary and fiscal policies is important, it’s not the sole focus.

- Financial System Stability: A robust and well-regulated financial system is essential for channeling savings into productive investment and fostering economic growth.

- Policy Measures: This could involve:

- Regulation: Implementing regulations to prevent excessive risk-taking in the financial sector and guard against future financial crises.

- Stress Testing: Regularly stress testing financial institutions to assess their resilience to economic shocks.

- Transparency: Enhancing transparency in financial markets to promote investor confidence and efficient resource allocation.

3. Data-Driven Policymaking —

- Beyond Traditional Indicators: Traditional economic indicators like GDP might not capture the full picture of economic well-being, particularly regarding income inequality and environmental sustainability.

- Embracing New Data Sources: Utilizing real-time data like consumer spending patterns, online job postings, and satellite imagery to gain a more nuanced understanding of economic conditions.

- Advanced Economic Models: Developing and employing advanced economic models that incorporate these new data sources to assess the potential impact of policy decisions.

Building Resilience:

These potential solutions aim to equip policymakers with a more flexible and data-driven toolkit. The focus on financial stability and a hybrid approach to monetary and fiscal policy can foster more resilient economies. Additionally, embracing new data sources and advanced economic models can improve policy decision-making in a rapidly changing world. The road ahead will likely involve continuous adaptation and innovation as policymakers navigate the evolving economic landscape.

Fiscal and Monetary Policy Working Together — The limitations of both monetarism and Keynesianism, particularly in light of recent crises, have fueled discussions around integrating fiscal and monetary policy. This approach aims to achieve a more coordinated and effective response to economic challenges. Here’s a closer look at the potential benefits and drawbacks of this integration:

Advantages —

Enhanced Policy Effectiveness: By working in tandem, fiscal and monetary policy can potentially achieve a more powerful and targeted impact on the economy. For instance, during a recession, expansionary fiscal policy (increased government spending) could be coupled with accommodative monetary policy (lower interest rates) to stimulate aggregate demand more effectively.

- Reduced Policy Conflicts: Friction can sometimes arise between fiscal and monetary policy goals. Integration can help ensure these policies complement each other, minimizing conflicting signals sent to the market.

- Improved Communication: Closer collaboration between central banks and governments can lead to more transparent and unified communication of economic policy direction, fostering greater market confidence.

Challenges and Considerations:

- Institutional Independence: Central banks are often designed to be independent of political influence. Excessive integration could compromise this independence, potentially leading to politicized monetary policy decisions.

- Moral Hazard: If governments know central banks will always bail them out by printing money to finance excessive spending, they might be less fiscally responsible, leading to higher inflation and debt in the long run.

- Implementation Complexity: Coordinating fiscal and monetary policy effectively requires a high degree of trust and cooperation between often-bureaucratic institutions. This can be challenging to achieve in practice.

Finding the Optimal Balance:

While full-fledged integration of fiscal and monetary policy has its drawbacks, there are ways to achieve a more coordinated approach:

- Memorandums of Understanding (MOUs): Central banks and governments can establish formal agreements outlining broad policy objectives and communication protocols.

- Policy Frameworks: Developing frameworks that encourage both fiscal and monetary authorities to consider the other’s actions when making policy decisions.

- Enhanced Communication: Regular dialogue and information sharing between central banks and governments can foster a more unified approach.

The concept of integrating fiscal and monetary policy remains a topic of debate among economists. While the potential benefits of a more coordinated approach are undeniable, the challenges of implementation and safeguarding central bank independence cannot be ignored. The most likely path forward might involve a combination of strategies, fostering closer communication and collaboration without compromising institutional independence. As the global economy continues to evolve, the debate on how to best integrate these policies will likely remain at the forefront of economic discourse.

Conclusion — The debate between Monetarism and Keynesianism has been a cornerstone of macroeconomic thought for decades. However, the complexities of the 21st-century economy necessitate a reevaluation of these traditional approaches.

Monetarism’s rigid rules-based framework may struggle to address the dynamic nature of modern financial markets and global interconnectedness. Keynesianism’s focus on active intervention, while valuable, requires careful consideration to avoid unintended consequences.

The path forward likely lies in a more nuanced approach. A framework that incorporates elements of both schools of thought, with a focus on long-term monetary stability alongside discretionary adjustments during economic fluctuations, could prove more effective. Furthermore, a data-driven approach that utilizes real-time economic information and advanced models can inform more precise policy decisions.

The challenges of income inequality, environmental sustainability, and technological disruption add further layers of complexity to the economic landscape. Policymakers must not only manage aggregate demand but also consider these emerging issues to ensure sustainable and inclusive economic growth.

The future of economic policy lies in adaptability and innovation. By acknowledging the limitations of traditional economic thought and embracing a more flexible and evidence-based approach, policymakers can navigate the complexities of the modern era and promote long-term economic prosperity.

Thanks.

Leave a comment