How Unified Payment Interface (UPI) is Transforming India’s Financial Landscape and Digital Public Infrastructure?

Credit availability plays an important role in economic system. As Fin-Tech industry is expanding at very fast rate not only in India but also world wide credit creation is important factor in every industrial framework. As 4G network expanded in India after 2016 we saw a massive boost in digital public infrastructure especially in Fin-Tech sector. And Universal Payment System or UPI has crucially important to its development.

Cash has long been the king in India. However, the recent years have witnessed a dramatic shift towards digital payments, driven largely by the innovation of the Unified Payment Interface (UPI). This single mobile application has emerged as a game-changer, not just for individuals and businesses, but for the entire financial ecosystem of the country. This article delves into the transformative impact of UPI on India’s financial landscape and digital public infrastructure. We’ll explore how UPI has fostered financial inclusion, revolutionized the way people conduct transactions, and empowered the growth of the fintech industry. By examining the seamless integration of UPI with government initiatives, we’ll further analyze how it is laying the foundation for a robust digital public infrastructure in India.

Financial Inclusion Revolution: How UPI Bridges the Gap in India —

Prior to the introduction of the Unified Payments Interface (UPI) in India, a significant portion of the population lacked access to formal financial services. This exclusion created a barrier to economic participation and hindered financial security for millions. However, UPI’s user-friendly design and mobile-first approach have revolutionized financial inclusion in India, bringing millions into the digital payments ecosystem.

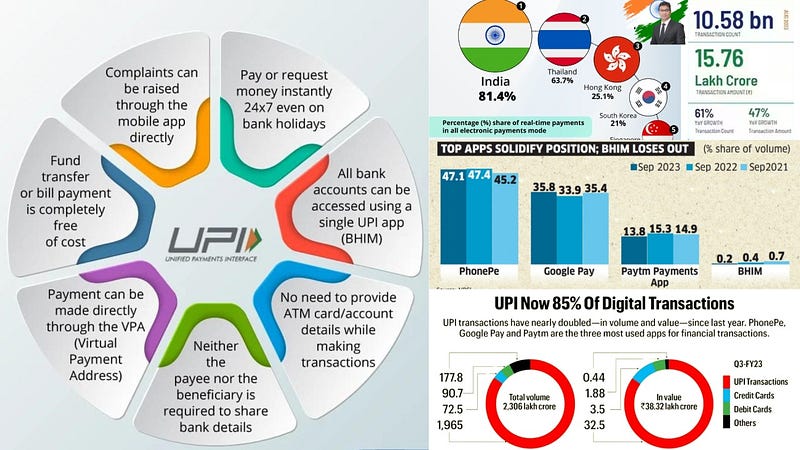

One of the key features of UPI that has played a major role in financial inclusion is the concept of Virtual Payment Addresses (VPAs). Unlike traditional bank account numbers, which can be long and complex, VPAs function like user-generated nicknames. These nicknames can be a person’s name, phone number, or any other easily remembered combination of letters and numbers. This eliminates the need for manual entry of lengthy bank details, a hurdle that often discouraged people, particularly those unfamiliar with technology, from adopting digital payments. With VPAs, sending and receiving money becomes as simple as sending a text message, making UPI an accessible tool for everyone regardless of their technical expertise.

Furthermore, UPI empowers small businesses, especially street vendors who are the backbone of India’s informal economy. Traditionally, accepting digital payments required expensive Point-of-Sale (POS) machines, which were often out of reach for these small businesses due to their cost and maintenance requirements. UPI, however, leverages the ubiquity of smartphones. With a UPI app installed on their phone, any vendor can instantly receive digital payments from customers. This not only eliminates the need for cash transactions but also opens doors for wider customer reach, potentially boosting their business.

In brief, UPI has emerged as a game-changer for financial inclusion in India. By simplifying transactions through VPAs and removing the barrier of expensive POS machines, UPI has empowered millions to participate in the digital economy. This not only fosters financial security for individuals but also injects vibrancy into the small business sector, ultimately contributing to India’s economic growth.

UPI: Transforming the Way We Transact in India — The Unified Payments Interface (UPI) has ushered in a new era of convenience and efficiency in how Indians conduct daily transactions. It has fundamentally changed the way people manage their money, replacing cumbersome traditional methods with a seamless digital experience.

One of the most impactful features of UPI is instant money transfers. Unlike traditional interbank transfers that can take hours or even days to complete, UPI facilitates real-time movement of funds between accounts. This not only eliminates the wait but also provides instant confirmation for both parties involved, a significant improvement over cash or cheque payments.

Furthermore, UPI goes beyond simple money transfers, offering a one-stop solution for various financial needs. Users can pay bills for utilities, mobile recharge, and other services directly through UPI apps. This eliminates the need for remembering due dates, standing in queues at physical bill payment locations, or relying on paper bills altogether. It streamlines the bill payment process, saving time and effort.

Adding another layer of convenience, UPI empowers users to make payments using QR codes. Merchants simply display a unique QR code, which users scan using their UPI app to initiate the transaction. This contactless payment method is not only fast and secure, but it also eliminates the need for carrying cash or swiping cards.

The rise of peer-to-peer (P2P) transactions is another significant aspect of UPI’s transformative impact. Splitting bills among friends, paying rent to a roommate, or reimbursing a colleague can now be done instantly via UPI, fostering a cashless society. This not only eliminates the need for physical exchange of cash but also creates a clear digital record of the transaction.

The widespread adoption of UPI has a two-fold impact: reducing cash handling costs and increasing transparency. As cash usage declines, businesses and individuals save money associated with security, transportation, and management of physical currency. Additionally, UPI transactions leave a digital footprint, making it easier to track financial activities and potentially reducing instances of tax evasion and black money circulation.

UPI system has revolutionized the way people conduct daily transactions in India. By offering instant transfers, seamless bill payments, and QR code-based payments, UPI promotes a cashless and convenient financial ecosystem. The rise of P2P transactions and the reduction in cash handling costs further solidify UPI’s transformative role in the Indian economy.

UPI: Fueling the Fintech Boom in India — The emergence of the Unified Payments Interface (UPI) has not only revolutionized individual transactions but has also served as a major catalyst for the growth of the Indian fintech industry. UPI’s open architecture and its widespread adoption have created fertile ground for innovation in financial services, fostering a vibrant ecosystem of players.

One of the key strengths of UPI is its open architecture. Unlike closed systems controlled by a single entity, UPI allows various players, including banks, payment service providers (PSPs), and fintech startups, to seamlessly integrate with the platform. This fosters healthy competition and collaboration, driving innovation in the financial services sector. Banks can leverage their existing infrastructure and customer base, while PSPs and fintech startups bring agility and fresh ideas to the table.

This open environment has led to a surge in new financial services tailored to the needs of the Indian market. For instance, UPI has enabled the growth of microloan providers. These fintech companies can leverage UPI’s infrastructure to offer small, instant loans to individuals who may not have access to traditional banking services. Similarly, UPI has facilitated the rise of digital wallets, which allow users to store money electronically and make payments conveniently. These wallets often offer additional features like cashback rewards and loyalty programs, further incentivizing digital transactions.

Furthermore, UPI’s reach has opened doors for innovation in wealth management solutions. Fintech startups are now developing user-friendly platforms that allow individuals to invest in stocks, mutual funds, and other financial instruments directly through their mobile phones. UPI integration enables seamless and secure transfer of funds for these investments, making wealth management more accessible to a broader audience.

It has played a pivotal role in propelling the Indian fintech industry forward. Its open architecture has fostered a collaborative environment where banks, PSPs, and fintech startups can innovate and develop new financial services. This has led to the emergence of microloans, digital wallets, and accessible wealth management solutions, catering to the diverse needs of the Indian population. As UPI continues to grow, it is poised to shape the future of financial services in India.

UPI: The Bedrock of India’s Digital Public Infrastructure — The Unified Payments Interface (UPI) transcends its role as a mere payment system. It has become a critical component of India’s digital public infrastructure (DPI), a network of open and interoperable platforms that power various digital services for citizens. UPI’s seamless integration with government initiatives and its potential for broader applications solidify its position as a cornerstone of India’s digital transformation.

One of the most impactful integrations of UPI is with the government’s Direct Benefit Transfer (DBT) programs. These programs aim to deliver subsidies and social welfare benefits directly to beneficiaries’ bank accounts. UPI acts as a secure and efficient channel for these transfers, ensuring transparency and minimizing leakages associated with traditional cash-based distribution systems. This empowers the government to deliver aid directly to those in need, fostering financial inclusion and reducing administrative costs.

Beyond DBT, UPI holds immense potential for various e-governance applications. For instance, citizens could potentially use UPI to pay for government services like passport renewals, driving license renewals, or utility bill payments. This would streamline service delivery, reduce queues, and enhance transparency within government agencies. UPI’s secure and user-friendly interface could also revolutionize tax payments, allowing individuals and businesses to file and pay taxes electronically with greater ease.

The significance of UPI lies in its contribution to building a more inclusive and efficient digital economy in India. By enabling secure and instant digital transactions for everyone, regardless of their socioeconomic background, UPI empowers individuals to participate actively in the digital marketplace. This fosters financial inclusion and creates a level playing field for small businesses to accept digital payments, boosting their reach and growth potential.

UPI’s integration with India’s digital public infrastructure extends far beyond facilitating everyday transactions. It plays a critical role in delivering social welfare programs efficiently, streamlining e-governance services, and fostering a more inclusive digital economy. As India continues on its digital journey, UPI is poised to remain a central pillar of this transformation.

Security, Future Potential — While UPI offers immense convenience, security remains a paramount concern for users. Here are some key security features built into UPI:

- Two-Factor Authentication (2FA): UPI transactions require both a mobile PIN and a virtual PIN (UPI PIN) for authorization, adding an extra layer of security.

- Virtual Payment Addresses (VPAs): VPAs mask sensitive bank account details, reducing the risk of exposing them during transactions.

- Encrypted Communication: UPI utilizes secure communication protocols to ensure data privacy during transactions.

Looking ahead, UPI has the potential to revolutionize financial services even further:

- Offline Payments: Integration of Near Field Communication (NFC) technology could enable offline UPI payments, expanding its reach to areas with limited internet connectivity.

- UPI-based Credit Options: Future iterations of UPI could introduce features like micro-credit or instant credit lines, providing users with greater financial flexibility.

UPI has emerged as a transformative force in India’s financial landscape. Its user-friendly interface, instant transactions, and open architecture have empowered millions to participate in the digital economy. From promoting financial inclusion to fostering innovation in the fintech sector, UPI’s impact is undeniable. As it continues to evolve and integrate with new technologies, UPI is well-positioned to shape the future of financial services in India, driving a more inclusive, efficient, and secure digital financial ecosystem.

Conclusion — The Unified Payments Interface (UPI) has woven itself into the fabric of India’s financial landscape, acting not just as a payment system, but as a cornerstone of the nation’s digital public infrastructure. By fostering financial inclusion, empowering small businesses, and fueling fintech innovation, UPI has fundamentally transformed the way Indians manage their money. Its seamless integration with government initiatives and its potential for future advancements solidify its position as a key driver of India’s digital transformation. As UPI continues to evolve, it holds immense promise for shaping a more inclusive, efficient, and secure financial future for India.

Leave a comment