How the Fed’s Rate Cut Impacts Emerging Market Monetary Policies ?

Recently in the September meeting the Federal Reserve chair Jerome Powell cut interest rate by 50 basis points as US’s inflation stood at 2.2 percent which is still high at Federal Reserve 2% target.

As Central bank plays important role in managing the supply of money and maintaining stability in the economy. Many of the central banks already followed the path of federal reserve’s path of cutting interest rates specifically Euro zone area and Emerging Market Economies.

Federal Reserve chair told that “the September decision reflects our growing confidence that, with an appropriate recalibration of our policy stance, strength in the labor market can be maintained in a context of moderate economic growth and inflation moving sustainably down to 2 percent”.

To understand why the US Federal Reserve and many other several central banks cut interest rates and how it affects the Emerging market economic policies it is imperative to understand the economic situations after the outbreak of COVID-19 Pandemic and geopolitical tensions — Russia — Ukraine War which affects the rise in food prices in the international market.

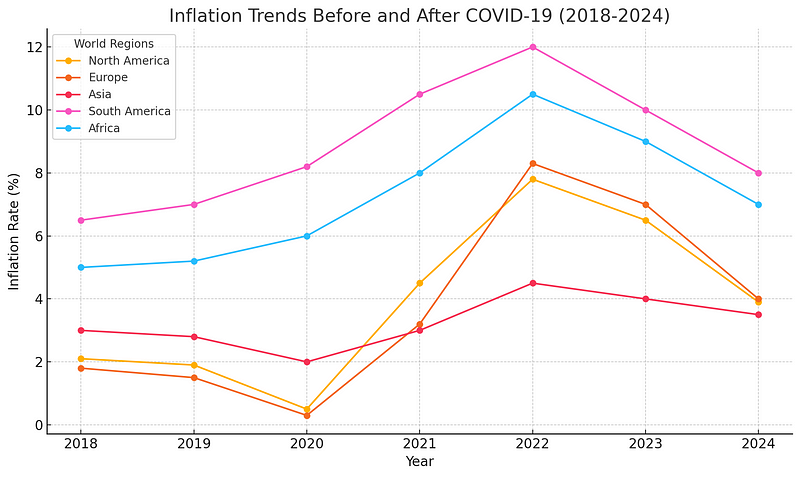

The following chart shows the inflation trends before and after the COVID-19 from 2018 to 2024 –

The following chart illustrates inflation trends from 2018 to 2024 for different regions –

Inflation rates in North America exhibited relative stability in the pre-pandemic years, with a modest fluctuation between 1.9% and 2.1%. However, in 2020, inflation decreased to 0.5% as the COVID-19 pandemic caused widespread economic contraction. By 2021, inflation surged to 4.5%, primarily due to fiscal stimulus, supply chain disruptions, and rising consumer demand. The inflationary peak was observed in 2022 at 7.8%, before moderating to 6.5% in 2023, and further decreasing to 3.9% in 2024 as supply chains stabilized and monetary policy tightened.

Similar to North America, Europe experienced low and stable inflation in the years preceding the pandemic, with rates of 1.8% and 1.5% in 2018 and 2019, respectively. In 2020, inflation fell to 0.3% during the early stages of the pandemic. However, as economic recovery gained momentum in 2021, inflation rose to 3.2%, accelerating significantly in 2022 to 8.3% due to the global energy crisis and supply shortages. By 2024, inflation had reduced to 4.0%, though it remained above pre-pandemic levels.

In Asia, inflation followed a relatively moderate path compared to other regions. Pre-pandemic inflation ranged from 2.8% to 3.0%, with a slight decline to 2.0% in 2020 as economic activity slowed. By 2021, inflation began rising again, reaching 3.0%, driven by higher commodity prices and supply chain disruptions. In 2022, inflation increased to 4.5%, but by 2024, it stabilized at 3.5%, reflecting more controlled economic recovery and a less aggressive inflationary cycle than in Western economies.

South America experienced higher inflation rates throughout the period. Prior to the pandemic, inflation rates were already elevated, with 6.5% and 7.0% recorded in 2018 and 2019, respectively. The pandemic exacerbated existing economic vulnerabilities, driving inflation to 8.2% in 2020 and further to 10.5% in 2021. Inflation peaked at 12.0% in 2022, reflecting severe economic disruptions, particularly in countries like Argentina. Although inflation moderated slightly to 10.0% in 2023 and 8.0% in 2024, it remained significantly above pre-pandemic levels.

In Africa, inflation was comparatively high even before the pandemic, with rates of 5.0% and 5.2% in 2018 and 2019, respectively. The region saw a notable increase in inflation during the pandemic, with rates reaching 6.0% in 2020 and further accelerating to 8.0% in 2021. Inflation peaked at 10.5% in 2022, driven by supply chain disruptions and global commodity price shocks. By 2024, inflation had moderated to 7.0%, yet it continued to surpass pre-pandemic figures, reflecting ongoing structural economic challenges.

Now this graph suggested that inflation had surged after the outbreak of COVID-19 pandemic due to the supply chain disruptions and the ongoing Russia-Ukraine war which leads to the rise in food and high energy prices.

Therefore, to tame the inflation central banks using affective monetary policy instruments like reducing supply of money in the economy with cutting interest rate which increases the borrowing costs. Furthermore, other policy instruments of the central banks like open market operations, discount rate, reserve requirements and quantitative easing also plays an important role in controlling the inflation in the economy.

What are the impact of rate cut to Emerging Market Economies?

USA played an important role in the world economic system and the Dollar’s position in the international financial markets is crucial to analyzing the financial markets. Due to enormous spread of globalization and rapidly expanding A.I. based technologies affecting the developed and underdeveloped world. Therefore, the policy frameworks of the Federal Reserve affects the monetary policy decisions of both the developed and developing countries.

The following points illustrates the effects of Fed’s rate cut on the Emerging Market Economies –

1) Currency Appreciation: When the Federal Reserve cuts interest rates, it often leads to a depreciation of the U.S. dollar. This can cause emerging market currencies to appreciate relative to the dollar. This is because investors tend to shift their funds from the U.S. to emerging markets seeking higher returns, increasing demand for the emerging market currencies.

2) Capital Inflows: Lower U.S. interest rates can attract capital inflows to emerging markets. Investors may seek higher yields offered by emerging market bonds and stocks. These inflows can provide a boost to emerging market economies by financing investment projects and infrastructure development. However, excessive capital inflows can also lead to asset price bubbles and economic overheating.

3) Inflationary Pressures: A stronger emerging market currency can lead to inflationary pressures. When the currency appreciates, imports become cheaper, putting downward pressure on domestic prices. However, if domestic demand is strong and supply chains are constrained, this can lead to inflationary pressures. Additionally, if the central bank allows the currency to appreciate too rapidly, it can hurt exports and slow down economic growth.

4) Debt Servicing: For emerging market countries with foreign-currency-denominated debt, a stronger currency can be a double-edged sword. On the one hand, it reduces the cost of servicing the debt in terms of the domestic currency. On the other hand, if the country’s exports are denominated in foreign currency, a stronger currency can make them less competitive in international markets, reducing export earnings and potentially straining debt servicing capacity.

Monetary Policy Response:

Emerging market central banks have several options to counteract the effects of a Fed rate cut. These include:

- 1) Raising Interest Rates: By increasing interest rates, central banks can make their currencies more attractive to investors, helping to prevent excessive currency appreciation.

- 2) Intervening in the Foreign Exchange Market: Central banks can sell their foreign currency reserves to buy back their domestic currency, helping to prevent excessive appreciation.

- 3) Capital Controls: In some cases, central banks may impose capital controls to limit the inflow of foreign capital and prevent asset price bubbles.

- 4) Macroprudential Measures: Central banks can implement measures to strengthen the financial system and reduce systemic risk, such as increasing capital requirements for banks or tightening lending standards.

The appropriate policy response will depend on the specific circumstances of each emerging market economy, including its level of economic development, the structure of its economy, and the nature of its external vulnerabilities.

Potential Risks and Challenges of Fed Rate Cuts on Emerging Markets –

Currency Volatility:

A Fed rate cut can lead to increased currency volatility in emerging markets. As investors shift their funds to emerging markets seeking higher returns, it can create a mismatch between supply and demand for the emerging market currencies. This can lead to sudden and sharp movements in exchange rates, which can create uncertainty and disrupt economic activity.

Asset Bubbles:

The influx of capital into emerging markets can fuel asset price bubbles. When investors are optimistic about the future prospects of an emerging market economy, they may be willing to pay higher prices for assets such as stocks, bonds, and real estate. This can create a bubble that is unsustainable and may eventually burst, leading to economic losses and financial instability.

Economic Overheating:

If emerging market economies are not able to manage the influx of capital effectively, they may experience economic overheating. Excessive capital inflows can lead to rapid credit growth, inflation, and asset price bubbles. These conditions can create a macroeconomic imbalance that is difficult to correct and can increase the risk of a financial crisis.

To mitigate these risks, emerging market central banks can implement a variety of policies, including:

- Macroprudential Measures: These measures aim to strengthen the financial system and reduce systemic risk, such as increasing capital requirements for banks or tightening lending standards.

- Capital Controls: In some cases, central banks may impose capital controls to limit the inflow of foreign capital and prevent asset price bubbles.

- Currency Intervention: Central banks can intervene in the foreign exchange market to smooth out excessive currency fluctuations.

- Monetary Policy Tightening: If the economy is overheating, central banks can raise interest rates to slow down economic activity and reduce inflationary pressures.

By carefully managing these risks, emerging market economies can reap the benefits of capital inflows while minimizing the potential negative consequences.

Conclusion — The Federal Reserve’s interest rate cuts have a significant impact on emerging market economies. While these cuts can provide a short-term boost to economic growth by attracting capital inflows and lowering borrowing costs, they also pose several risks. Currency appreciation, inflationary pressures, and debt servicing challenges can create difficulties for emerging market countries.

To navigate these challenges effectively, emerging market central banks need to carefully monitor economic conditions and implement appropriate policy measures. This may include raising interest rates, intervening in the foreign exchange market, and implementing capital controls. By adopting a balanced approach, emerging market economies can mitigate the potential negative effects of Fed rate cuts and harness the opportunities they present.

Thanks.

Leave a comment