Commercial Banks as Financial Intermediaries: Paving the Way for Capital Formation and Sustainable Economic Growth

The efficient functioning of a nation’s financial system is widely recognized as a cornerstone of its economic development and stability. Within this intricate system, commercial banks occupy a pivotal position, acting as the primary conduits through which financial resources are mobilized and allocated across various sectors of the economy. Their traditional role extends beyond mere deposit-taking and lending; they serve as critical financial intermediaries, bridging the gap between surplus and deficit units, thereby facilitating the transformation of idle savings into productive investments. This intermediation function is not merely transactional; it is foundational to the process of capital formation, which, in turn, is indispensable for sustained economic growth.

Despite the pervasive influence of commercial banks on economic activity, the precise mechanisms and the extent to which they stimulate capital formation and contribute to sustainable economic growth remain subjects of ongoing academic inquiry and policy debate. Modern economies are characterized by complex financial landscapes, where banks operate amidst evolving regulatory frameworks, technological advancements, and global economic shifts. Understanding their dynamic role in fostering investment is crucial for policymakers aiming to design effective strategies for economic expansion and resilience.

This article posits that commercial banks are indispensable financial intermediaries whose multifaceted operations are instrumental in paving the way for robust capital formation and, consequently, sustainable economic growth. We argue that their unique capacity to aggregate dispersed savings, assess and manage risk, and channel funds towards productive ventures directly fuels the investment necessary for industrial expansion, infrastructural development, and technological innovation. Furthermore, their role in providing liquidity and facilitating payment systems underpins the efficiency of economic transactions, creating an environment conducive to long-term prosperity.

To substantiate this argument, this paper will first delineate the theoretical underpinnings of financial intermediation and its link to economic growth. Subsequently, it will explore the various channels through which commercial banks perform their critical functions, including credit allocation, risk transformation, maturity transformation, and the provision of financial services. We will then examine empirical evidence illustrating the positive correlation between a well-developed banking sector and indicators of capital formation and economic growth. Finally, the article will discuss the policy implications arising from this analysis, suggesting strategies to optimize the intermediating role of commercial banks to ensure a more stable and sustainable path to economic development.

The Foundational Role of Financial Intermediation by Commercial Banks —

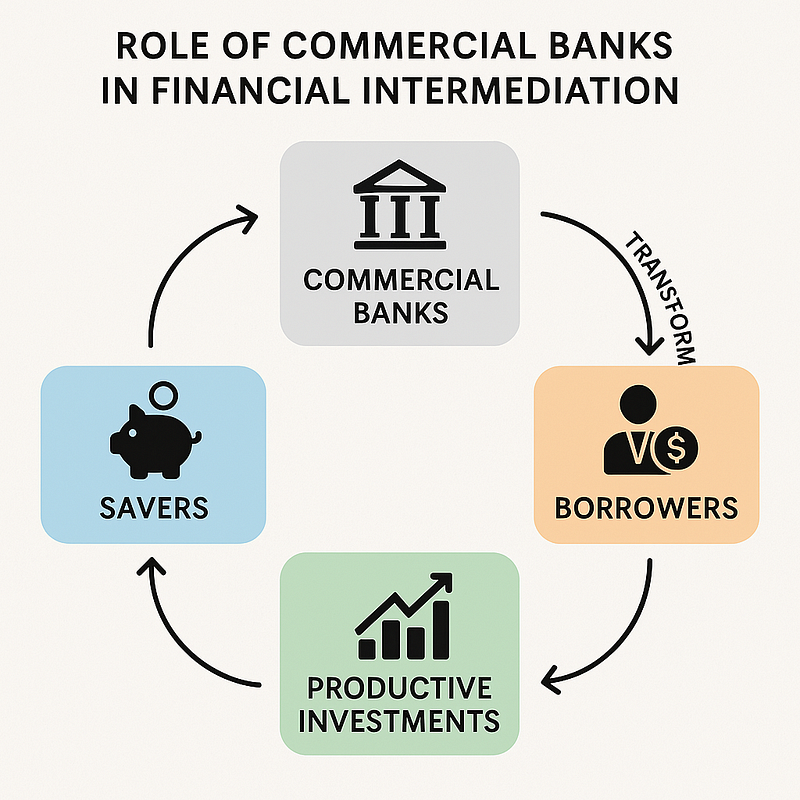

Commercial banks are not merely institutions that lend money — they serve a foundational role in financial intermediation, a process vital to the functioning of a modern economy. Through financial intermediation, banks channel funds from savers to borrowers, transforming idle savings into productive investments. This function is central to capital formation, employment generation, and overall economic development.

1. Mobilizing Savings

Commercial banks aggregate small and scattered savings from households, businesses, and institutions. In the absence of such institutions, much of the money would remain unutilized, stashed in physical assets or lying idle.

- Banks offer safety, liquidity, and interest income, encouraging people to deposit surplus funds.

- These deposits form the raw material for the banking system’s credit operations.

2. Channeling Funds to Investment

Banks do not hoard the deposits they collect. Instead, they allocate them to sectors where capital is most needed — be it for entrepreneurs starting businesses, farmers buying equipment, or industries expanding production.

- They assess creditworthiness, risk, and returns, making them effective gatekeepers of capital allocation.

- Loans and advances extended to businesses and individuals convert passive savings into productive capital.

3. Facilitating Capital Formation

Capital formation is the accumulation of real capital assets such as machines, tools, factories, and infrastructure. It is a key determinant of long-term economic growth.

- By granting credit for productive purposes, banks stimulate investment in capital goods.

- Increased investment leads to enhanced productive capacity, employment, and national income.

4. Supporting Economic Growth

By transforming financial resources into physical capital, banks act as a catalyst for economic growth:

- Entrepreneurial Support: By funding innovations and startups.

- Infrastructure Development: Financing roads, bridges, power plants.

- Sectoral Growth: Prioritizing credit to sectors like agriculture, MSMEs, and manufacturing.

5. Ensuring Efficient Allocation of Resources

Through credit appraisal, monitoring, and risk management, commercial banks ensure that funds are not just deployed, but deployed efficiently.

- This prevents capital misallocation, reduces wasteful spending, and enhances productivity.

- Efficient capital allocation means higher returns to investors and sustained growth in GDP.

Mechanisms of Capital Formation through Banks —

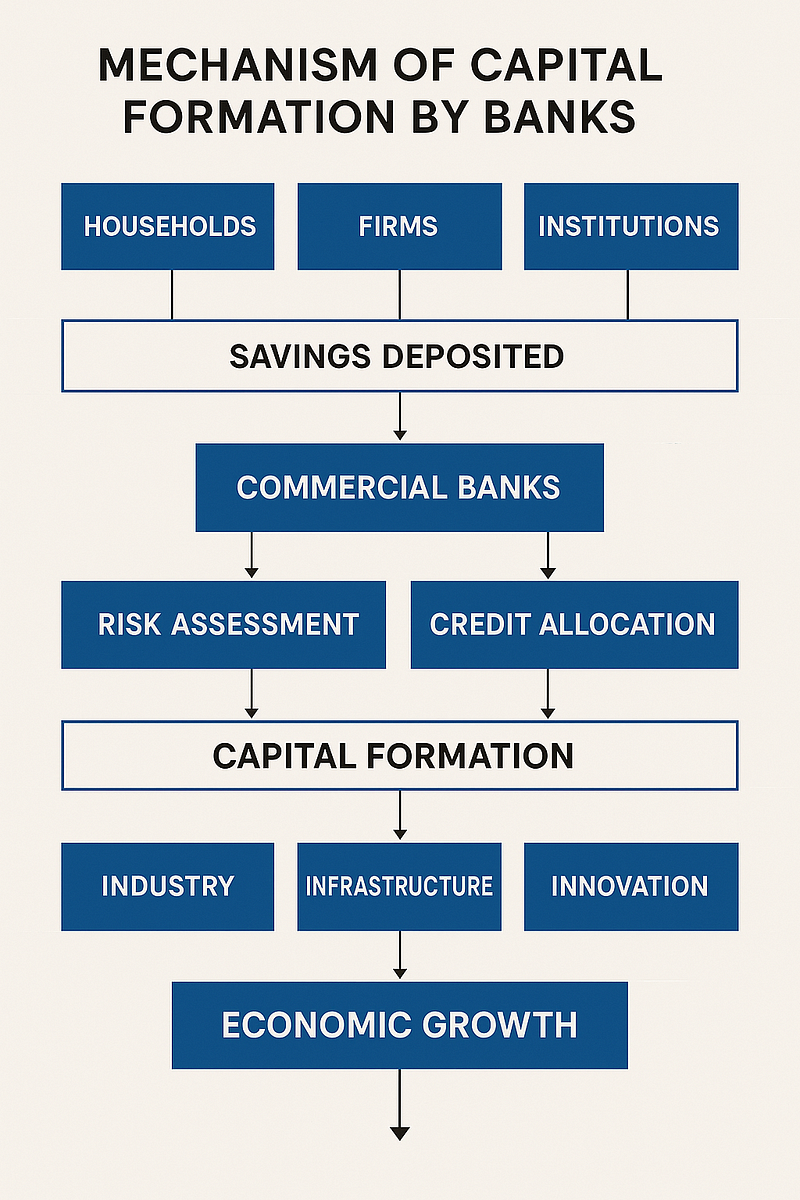

1. Aggregation of Dispersed Savings

Banks play a vital role in mobilizing savings from millions of households, small businesses, and institutions. These savings are often small and scattered but collectively form a large pool of investable funds.

Mechanisms:

- Deposit Schemes: Savings accounts, fixed deposits, recurring deposits.

- Financial Inclusion: Extending banking to rural and remote areas through branches, digital banking, Jan Dhan Yojana, etc.

- Trust and Liquidity: Offering safety, liquidity, and moderate returns encourages deposit growth.

Impact:

- Transforms idle funds into productive capital.

- Promotes a culture of saving, especially in developing economies.

2. Risk Assessment and Management

Banks act as intermediaries by evaluating the creditworthiness of borrowers and managing various types of risks associated with lending and investment.

Mechanisms:

- Credit Appraisal: Analyzing financial statements, collateral, credit history, and business plans.

- Diversification: Lending across sectors (agriculture, industry, housing, services) and regions to minimize portfolio risk.

- Regulatory Compliance: Following Basel norms, provisioning for NPAs, risk-weighted assets.

- Insurance and Guarantees: Use of credit guarantees, collateralized loans, or risk-sharing arrangements.

Impact:

- Encourages responsible lending.

- Reduces systemic risks and enhances trust in the financial system.

3. Efficient Allocation of Capital to Productive Ventures

Banks use the mobilized savings to channel funds to sectors where they yield the highest economic returns, ensuring optimal capital formation.

Key Areas of Allocation:

- Industrial Expansion:

- Term loans for setting up or expanding manufacturing units.

- Working capital finance for day-to-day operations.

- Project finance for large-scale industrial projects.

2. Infrastructure Development:

- Funding for roads, ports, railways, power plants, and digital infrastructure.

- Public-Private Partnership (PPP) models.

- Long-term loans through infrastructure-focused financial institutions and bank consortia.

3. Technological Innovation:

- Venture capital and startup funding (especially via bank-led NBFCs or SIDBI-backed schemes).

- Financing R&D and digital transformation of SMEs.

- Promoting fintech and digital ecosystems through innovation funds.

Mechanisms:

- Priority Sector Lending (PSL): Ensures credit access to agriculture, MSMEs, education, housing, etc.

- Sector-Specific Schemes: Like Mudra Loans, Start-up India, Stand-Up India.

- Project Appraisal & Monitoring: For efficient capital use and reducing bad loans.

Impact:

- Boosts GDP growth through enhanced productivity.

- Supports employment generation, innovation, and long-term development.

- Reduces regional and sectoral imbalances.

Contribution of Commercial Banks to Sustainable Economic Growth— Commercial banks play a crucial systemic role in ensuring that an economy not only grows, but does so in a sustainable, inclusive, and efficient manner. Their core functions — providing liquidity, facilitating payment systems, mobilizing savings, allocating credit, and managing risk — collectively support a stable financial infrastructure, which is the backbone of long-term development.

1. Providing Liquidity: Fuel for Economic Activity

Liquidity refers to the ease with which assets can be converted into cash without loss. Banks ensure that liquidity is always available for:

- Individuals: through savings accounts, overdrafts, and personal loans.

- Businesses: via working capital finance, cash credit, and trade finance.

- Governments: by managing treasury operations and public debt.

Impact on Sustainable Growth:

- Reduces transaction frictions in the economy.

- Prevents financial bottlenecks that can trigger recessions.

- Ensures economic resilience during shocks like pandemics or natural disasters.

2. Facilitating Efficient Payment Systems

Commercial banks maintain and operate modern, secure, and fast payment mechanisms — cheques, NEFT, RTGS, IMPS, UPI, credit/debit cards, mobile banking, and internet banking.

Impact on Sustainable Growth:

- Reduces transaction costs and time delays.

- Promotes transparency and reduces the shadow economy.

- Enables financial inclusion, especially for rural and remote populations.

- Supports digitalization and e-commerce, boosting efficiency and innovation.

3. Promoting Capital Allocation Efficiency

Through credit appraisal mechanisms, commercial banks ensure that funds are allocated to viable, sustainable projects with long-term benefits.

Impact:

- Prevents resource misallocation and non-performing assets (NPAs).

- Encourages green finance, infrastructure, and MSME growth.

- Supports economic sectors that contribute to environmental and social sustainability.

4. Stabilizing the Financial System

Banks operate under prudential norms, reserve requirements, and supervision by central banks, which creates a stable financial environment necessary for long-term investment and confidence.

Impact:

- Attracts foreign investment.

- Minimizes the risk of systemic crises.

- Supports macroeconomic stability — low inflation, steady growth, and stable currency.

5. Supporting Inclusive and Sustainable Development Goals (SDGs)

Modern commercial banks are increasingly aligning with the UN Sustainable Development Goals:

- Providing credit to women entrepreneurs, farmers, and green projects.

- Offering microfinance and promoting financial literacy.

- Encouraging savings and insurance to reduce vulnerability to economic shocks.

Key Functions of Commercial Banks —

Commercial banks are the cornerstone of financial intermediation, playing multiple roles that ensure efficient allocation of resources, risk management, and liquidity transformation. Their functions can be categorized into core intermediation roles and a broader range of financial services.

1. Credit Allocation

Commercial banks perform the crucial function of allocating credit by channeling funds from surplus units (savers) to deficit units (borrowers).

How it works:

- Banks collect deposits from individuals, businesses, and institutions.

- They assess creditworthiness and extend loans to those who can utilize capital productively — entrepreneurs, manufacturers, service providers, etc.

- Loans can be short-term (working capital) or long-term (capital investment).

Importance:

- Supports capital formation and enterprise development.

- Helps in sectoral development by targeting priority sectors like agriculture, MSMEs, infrastructure.

- Aids in balanced regional development when banks serve underserved areas.

2. Risk Transformation

Banks help manage and transform risk through mechanisms that protect both depositors and borrowers.

Key aspects:

- Risk Pooling: Banks pool funds from numerous depositors and diversify them across different borrowers and sectors.

- Credit Risk Management: Through credit appraisal, collateral, guarantees, and insurance mechanisms.

- Liquidity Risk Handling: Banks hold reserves and maintain capital adequacy to manage unexpected withdrawals or defaults.

Importance:

- Depositors face lower individual risk due to diversification.

- Borrowers gain access to credit without bearing the burden of finding individual investors.

3. Maturity Transformation

Commercial banks specialize in maturity transformation — the conversion of short-term liabilities into long-term assets.

How it works:

- Banks accept short-term deposits (e.g., savings, current accounts).

- They use these funds to issue long-term loans (e.g., housing loans, industrial finance).

- Use liquidity buffers, reserve ratios, and asset-liability management (ALM) to manage the mismatch.

Importance:

- Provides long-term funding for investment while giving depositors quick access to their funds.

- Smoothens consumption and investment flows, enhancing economic efficiency.

4. Provision of Financial Services Beyond Lending

Modern commercial banks offer a wide array of financial services that promote economic efficiency, financial literacy, and inclusion.

Key services:

- Deposit Services: Savings, current, and fixed deposits.

- Payment and Settlement: Cheque clearing, mobile banking, NEFT, RTGS, IMPS, UPI, cards.

- Foreign Exchange Services: Currency exchange, remittances, export-import financing.

- Wealth Management: Mutual funds, insurance, retirement planning.

- Advisory Services: Investment, mergers and acquisitions, credit counselling.

- Digital Banking: Net banking, mobile apps, digital wallets, fintech partnerships.

Importance:

- Facilitates cashless economy and financial inclusion.

- Encourages formalization of economic transactions.

- Helps consumers and businesses manage and grow their wealth efficiently.

Empirical Evidence Linking Banking Sector Development to Capital Formation and Economic Growth

1. Global Cross-Country Studies

A. King and Levine (1993) — Landmark Study

- Title: Finance and Growth: Schumpeter Might Be Right

- Sample: 80 countries over 1960–1989

- Key Findings:

- Higher levels of financial intermediation (measured by bank credit to private sector as % of GDP) are associated with higher real per capita GDP growth, capital accumulation, and productivity improvements.

- Financial development leads, rather than follows, economic growth.

B. Beck, Levine, and Loayza (2000)

- Study: Finance and the Sources of Growth

- Methodology: Panel data regression with controls for endogeneity

- Findings:

- Countries with better-developed financial systems enjoy faster economic growth.

- Strong banking systems improve resource allocation and accelerate capital formation through efficient mobilization of savings and credit allocation.

2. Regional Studies

B. Latin America — Calderón and Liu (2003)

- Data: 109 countries (1960–1994), using Granger causality analysis

- Findings:

- Causal relationship from financial development (especially banking depth) to economic growth.

- Improved banking access increases capital formation through higher investment rates.

B. Sub-Saharan Africa — Andrianaivo and Yartey (2010)

- Focus: Impact of banking sector development on growth and poverty reduction.

- Findings:

- Banking sector expansion led to higher gross capital formation and inclusive growth.

3. India-Specific Evidence

A. RBI Study (2020): Financial Intermediation and Growth

- Data Period: 1991–2018

- Findings:

- Banking sector reforms post-1991 contributed to:

- A rise in gross capital formation (from ~22% in 1990 to ~30% of GDP in early 2000s).

- Increased credit to infrastructure and industry.

- Growth in SMEs and rural credit access.

- Strong correlation between real GDP growth and banking credit growth.

B. Rajan and Zingales (1998) — Sectoral Evidence

- Concept: Finance-dependent sectors grow disproportionately faster in countries with advanced financial systems.

- Application in India:

- Post-liberalization, Indian manufacturing sectors heavily reliant on external finance grew faster in states with better banking infrastructure.

4. Case Studies

A. India’s Priority Sector Lending

- Directed credit to agriculture, MSMEs, and weaker sections.

- Increased rural capital formation and employment creation.

- NABARD and regional rural banks facilitated targeted investments.

B. Bank Branch Expansion in Rural India (Burgess and Pande, 2005)

- Study: Impact of bank branch expansion on poverty

- Findings:

- 1% increase in rural branches reduced poverty by 0.34%.

- Greater branch density led to higher rural savings and agricultural investment.

Policy Implications: Optimizing the Role of Commercial Banks in Investment and Economic Development — Commercial banks play a vital role in capital formation and the broader objective of economic development. In light of the empirical evidence demonstrating their impact, policymakers must adopt strategic interventions to enhance their effectiveness within evolving global and domestic financial contexts. The following are key actionable insights and policy strategies:

1. Strengthening Regulatory and Supervisory Frameworks

A sound regulatory environment is essential to ensure the stability and efficiency of the banking sector. Policymakers should adopt risk-based supervision and align domestic banking regulations with global standards such as Basel III+. Capital adequacy norms must be dynamic and reflective of systemic risks. Supervisory bodies should encourage the use of advanced credit appraisal techniques, including data analytics and artificial intelligence, to minimize defaults and strengthen credit quality.

2. Expanding Financial Inclusion to Deepen the Capital Base

Expanding access to banking services enhances the mobilization of domestic savings and promotes inclusive growth. Strategies should include extending the physical and digital presence of banks in rural and underserved areas, simplifying Know Your Customer (KYC) norms through digital solutions like Aadhaar-enabled authentication, and promoting financial literacy campaigns. Special attention must be given to the development of inclusive credit instruments targeting small farmers, women entrepreneurs, and micro-enterprises.

3. Facilitating Long-Term and Infrastructure Financing

Capital formation requires substantial long-term financing, particularly in infrastructure and capital-intensive sectors. Policymakers should incentivize banks to extend longer-tenure credit and support the creation of specialized infrastructure lending divisions. Strengthening coordination between commercial banks and development financial institutions can facilitate the financing of critical projects. Credit enhancement tools, such as government guarantees and risk-sharing mechanisms, should be utilized to mitigate the risk associated with long-term investments.

4. Promoting Technological Innovation and Digital Transformation

Digital banking and financial technologies can enhance the efficiency and reach of commercial banks. Policymakers should encourage the adoption of fintech innovations through regulatory sandboxes and foster open banking ecosystems. Banks must be supported in building robust digital infrastructure to deliver secure and user-friendly services. The integration of emerging technologies such as artificial intelligence, blockchain, and central bank digital currencies (CBDCs) should be guided by appropriate regulatory oversight.

5. Addressing Non-Performing Assets (NPAs) and Strengthening Credit Discipline

The effective management of NPAs is critical to maintaining credit flow and investor confidence. Early warning systems, real-time credit monitoring, and borrower scoring mechanisms must be institutionalized. The resolution process under the Insolvency and Bankruptcy Code (IBC) should be expedited, and the creation of professionally managed asset reconstruction companies must be encouraged. Lending policies should link future access to credit with borrower behavior and credit performance.

6. Aligning Banking Activities with Sustainable Development Goals (SDGs)

Commercial banks should be guided to align their lending practices with environmental and social objectives. Policymakers should promote green financing by offering incentives for projects in renewable energy, clean mobility, and sustainable agriculture. Environmental risk assessments must be integrated into lending criteria, and banks should be encouraged to adopt sustainability-linked loan frameworks. Climate-resilient banking will ensure that capital formation supports long-term environmental sustainability.

Addressing Modern Challenge — In today’s dynamic economic environment, commercial banks operate amidst a complex interplay of regulatory evolution, rapid technological advancements, and global economic shifts. These factors have significantly reshaped their role as financial intermediaries.

- Evolving Regulatory Frameworks

Banks are now subject to stricter regulations aimed at safeguarding financial stability. Compliance with international norms such as Basel III, anti-money laundering (AML) standards, and enhanced capital adequacy requirements has strengthened risk management practices. However, these regulations also impose constraints on credit expansion and raise the cost of compliance, requiring banks to balance stability with lending efficiency. - Technological Advancements

Digital transformation has revolutionized banking operations. The adoption of artificial intelligence, blockchain, mobile banking, and digital lending platforms has improved customer outreach, operational efficiency, and credit risk assessment. These innovations enhance the intermediation function by enabling banks to mobilize savings more effectively and extend credit through alternative data-driven methods, particularly to underserved populations. - Global Economic Shifts

Banks are increasingly influenced by global factors such as capital flow volatility, geopolitical tensions, inflationary pressures, and changes in trade dynamics. These developments affect interest rates, credit demand, and foreign exchange exposure. Additionally, climate change and the global push for sustainable finance are compelling banks to reorient their portfolios toward green investments and resilient lending practices.

Collectively, these modern challenges are redefining how banks perform their intermediation role. Institutions that adapt proactively by investing in compliance, embracing technology, and aligning with global trends are better positioned to support capital formation and foster inclusive, long-term economic development.

Conclusion — this article has meticulously explored the indispensable role of commercial banks as financial intermediaries in fostering capital formation and driving sustainable economic growth. We have argued that their functions extend far beyond the simplistic view of deposit-taking and lending, encompassing complex mechanisms that are fundamental to a healthy and expanding economy. By effectively bridging the divide between surplus-holding economic agents and deficit-spending productive units, commercial banks serve as the vital arteries through which financial capital flows, transforming latent savings into tangible investments.

Our analysis has underscored the multifaceted nature of this intermediation. Commercial banks are adept at aggregating fragmented savings, thereby achieving economies of scale in investment. Crucially, they perform essential risk transformation, diversifying and managing the inherent risks associated with lending, making investment opportunities more palatable for both savers and borrowers. Furthermore, their capacity for maturity transformation ensures that short-term deposits can finance long-term projects, a cornerstone of infrastructural development and industrial expansion. Beyond these core functions, their provision of liquidity and efficient payment systems lubricates the wheels of commerce, enhancing transactional efficiency and reducing systemic friction within the economy. The empirical evidence consistently supports a strong positive correlation between the depth and efficiency of the banking sector and a nation’s capacity for capital formation and sustained economic prosperity.

The enduring significance of commercial banks necessitates a continuous focus on optimizing their intermediating role. For policymakers, this implies the imperative of establishing and maintaining robust yet adaptive regulatory frameworks that balance financial stability with the encouragement of innovation and responsible risk-taking. Policies promoting financial inclusion are equally vital, ensuring that a broader segment of the population and small-to-medium enterprises (SMEs) gain access to the credit necessary for their growth, thereby fostering a more equitable distribution of economic benefits. Effective supervision is paramount to mitigate systemic risks and prevent financial crises that can derail capital formation and economic progress. Moreover, fostering a competitive banking environment can drive efficiency and better service provision, further enhancing the intermediation process.

As global economies continue to evolve, marked by rapid digitalization, the rise of fintech, and the increasing urgency of climate finance, the role of commercial banks will undoubtedly adapt. Future research should delve deeper into the specific impacts of these transformative forces on banking intermediation, exploring how traditional banks can leverage new technologies, integrate sustainable finance principles, and enhance their resilience in an increasingly volatile global landscape. Nevertheless, the fundamental premise remains: commercial banks, through their sophisticated intermediation, will continue to be central figures in paving the way for robust capital formation and, consequently, the achievement of sustainable and inclusive economic growth for nations worldwide.

Thanks.

Leave a comment